By Ayobami Ayorinde and Seyi Akinbodewa | For the first time in decades, Nigeria’s Federal Government has undertaken a comprehensive tax reform. The journey started with the announcement and inauguration of the Presidential Committee on Fiscal Policy and Tax Reforms, led by Mr. Taiwo Oyedele, a renowned tax expert.

President Bola Tinubu’s principal charge to the committee was to raise Nigeria’s revenue profile and improve the country’s competitiveness. At the inauguration of the committee in August 2023, President Tinubu declared: “Our aim is to transform the tax system to support sustainable development, while, at the same time, achieving a minimum of 18% Tax-to-GDP ratio within the next three years”[1]. After about two years of consultations, a spicy national debate and legislative treatment, four approved bills were presented to the president for his assent. The president appended his signature at a public event in June 2025, and by September 2025, the Federal Government disclosed that the new laws had been gazetted.

The signed and gazetted laws are:

- The Nigeria Tax Act (NTA) which is to provide a unified fiscal framework to govern taxation across Nigeria;

- The Nigeria Tax Administration Act (NTAA) which is to provide for the assessment, collection, and accounting for revenue accruing to the Federation, as well as to federal, state, and local governments, and also prescribe the powers and functions of tax authorities;

- The Nigeria Revenue Service (Establishment) Act (NRSEA) which is to repeal the Federal Inland Revenue Service Establishment Act No. 13 of 2007 and enact the Nigeria Revenue Service, which will be empowered to assess, collect, and account for revenues accruing to the Government of the Federation;

- The Joint Revenue Board (Establishment) Act (JRBEA) which is to establish the Joint Revenue Board, the Tax Appeal Tribunal, and the Office of the Tax Ombudsman for the harmonisation, coordination, and settlement of disputes arising from revenue administration in Nigeria.

Now that the new tax laws are in the public domain, this article reviews some of the promises made versus what has been delivered.

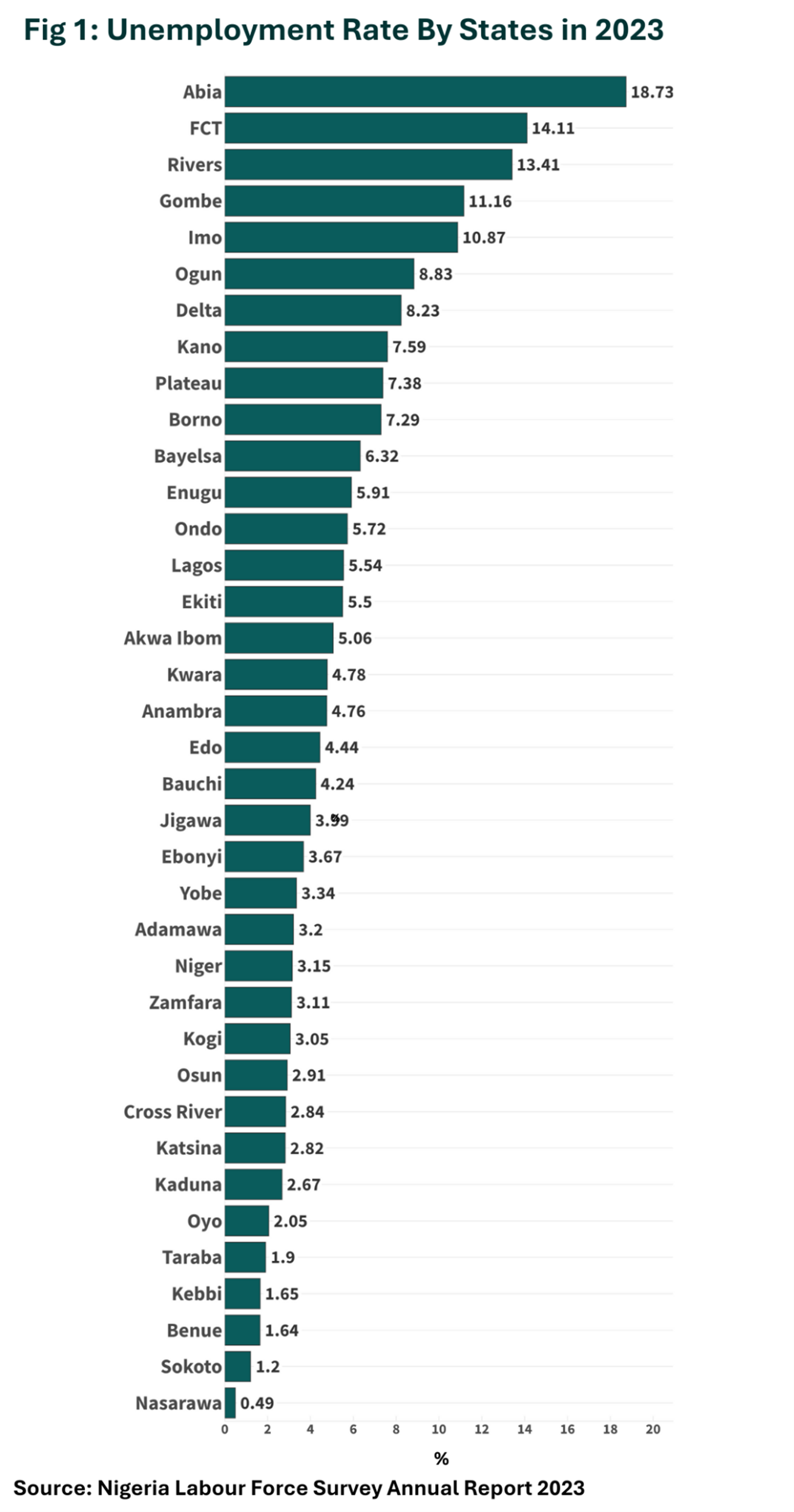

To start with, the need to strengthen Nigeria’s tax laws cannot be overstated. Nigeria has a revenue crisis that makes it increasingly difficult to fund its budget. But more than that, Nigeria’s tax collection lags behind its neighbours and peer countries. According to the African Tax Outlook Report of 2024, Nigeria’s tax-to-GDP ratio at 11.13% in 2023 was lower than the average of the 35 African countries at 15.12%[2].  Due to inadequate revenue from taxes and from other revenue sources, Nigeria struggles to generate enough for its needs and size and continues to resort to borrowing, which leads to a vicious cycle where debt servicing consumes a large share of government’s revenue. This was the backdrop to the tax reforms.

Due to inadequate revenue from taxes and from other revenue sources, Nigeria struggles to generate enough for its needs and size and continues to resort to borrowing, which leads to a vicious cycle where debt servicing consumes a large share of government’s revenue. This was the backdrop to the tax reforms.

A Mixed Outcome: Some Key Promises Delivered, Some Not

The government through the committee was ambitious and promised a number of reforms. However, going by the provisions in some of the Acts, a number of outcomes did not fully reflect the objectives that the committee set out at the beginning. For example, two of the most significant proposed tax rate changes did not materialise. It was proposed in the bills that the rate for the Company Income Tax (CIT) be gradually reduced from 30% to 25% over a two-year period. This move was intended to ease the burden on large businesses– one of the goals of the reforms. At 30%, Nigeria has one of the highest CIT rates in Africa, above countries like Egypt (22.5%), Ghana (25%) and South Africa (27%). However, the new tax laws kept CIT at 30% for large companies albeit with a provision to enable its reduction from 30% to 25% effective from a date as may be determined in an order by the president on the advice of the National Economic Council. Similarly, the proposal to increase the Value Added Tax (VAT) rate in phases from 7.5% in 2025 to 15% by 2030 was not approved. The objective of a proposed VAT increase was to raise more tax revenue. At 7.5%, Nigeria has the second-lowest VAT rate in Africa, higher only than Eritrea’s 5%. The government, through the committee, had earlier stated that the proposed increase in VAT rate would not lead to inflation[3] but concerns about inflation lingered. The decision to maintain the current VAT rate is understandable, especially given the economic pressures that followed the fuel subsidy removal and exchange rate unification in 2023, which triggered a period of high inflation. But it is also important to note that the rationale behind exempting essentials like food, education, and medical services from VAT was to cushion the impact of the planned increase in the VAT rate. Despite this concession, the government was not able to see the promise through. This in particular risks the objective of growing the country’s tax-to-GDP ratio significantly in the next three years.

The allocation of VAT revenue, particularly the horizontal sharing formula, which determines how VAT revenue is distributed among the states, was one of the most contentious issues before passage of the bills. The current formula is based on: 50% equality, 30% population and 20% derivation. It is noteworthy that in the early days of VAT, companies filed and paid taxes through their branch offices. However, because of the cumbersome process of deducting input VAT from output VAT, it shifted to a system of centralised filing through head offices. This created what is now known as the “Headquarters Effect,” where VAT paid by companies is tied to the company’s head office rather than where the business activity actually occurs[4]. However, this model was faulted by the committee for being skewed in favour of states like Lagos and Rivers, where many large corporations have their headquarters and remit their VAT. As such, the committee proposed a new formular of: 60% derivation (based on consumption and not attribution), and 20% each for equality and population. This was the most contentious part of bills submitted to the parliament.

After consultations with key stakeholders, especially governors under the aegis of the Nigerian Governors’ Forum (NGF), the allocation formula was eventually set at: 50% equality, 30% derivation (now tied to where goods and services are actually consumed) and 20% population. The current model now recognises that if a person buys a product in Yobe for example, even if the company that sold it is headquartered in Lagos, the VAT from that purchase will now be credited to Yobe, not Lagos. At the vertical level, which refers to how VAT is shared among the three tiers of government, the new arrangement now reduces the Federal Government’s share from 15% to 10%, the states’ share increases from 50% to 55%, while local councils’ share remains at 35%. The proposed change in the vertical sharing formula for VAT scaled through, though it means the Federal Government will get less of revenues from VAT. As things stand, this lower share will not be compensated by higher VAT rates. So, the FG is likely to get less revenues from VAT, an increasingly prominent revenue handle.

The establishment of the NRS to replace the FIRS and oversee the collection of taxes and the cost of revenue collection is a significant institutional reform. The rationale behind the change of name was that since tax revenues go into the Federation Account and are shared among the three tiers of government, having the service named after the country will reflect the collective ownership of tax revenue and the broader national interest it serves[5]. All things being equal, this should allow for greater efficiency in revenue collection. But there is still some uncertainty about how its responsibilities will be shared with some existing revenue-collecting agencies like the Nigerian Upstream Petroleum Regulatory Commission (NUPRC) which collects 4% of oil royalties. This ambiguity is concerning, given that in 2024 Oyedele promised a reduction in the cost of collection to as low as 1%[6]. When the Nigeria Revenue Service (Establishment) bill was submitted to the National Assembly, the cost of collection for NRS was proposed at 3%, thrice what Oyedele had promised. Interestingly, however, he final version of the Nigeria Tax Act grants NRS a 4% cut of total revenues collected, excluding petroleum royalties. This means that NRS is likely to receive a higher collection cost than FIRS, as the latter only receives 4% of non-oil revenue whereas NRS is billed to receive 4% of all revenues minus petroleum royalties (which is just a portion of oil revenue). This contradicts the committee's earlier vision of reduced collection costs. For the Nigerian Customs Service (NCS), the reintroduction of the unified 4% FOB charge which was signed into law in April 2023 as part of the Nigeria Customs Service Act (NCSA) 2023, is expected to eliminate the 7% cost of collection charged by the NCS. However, considering its recent suspension by the government, it remains to be seen how this would play out.

As part of the tax reforms, the many earmarked levies that companies used to pay have now been consolidated into a single 4% development levy. The goal is to simplify and harmonise the tax system. On the aggregate, this set of taxes have been slightly reduced. But this change means that businesses previously exempt from levies like NITDA and NASENI will now face an additional tax burden under the new levy. Currently, Nigerian resident companies, except small firms with a turnover of ₦25 million or less, are required under the TETFUND Act to pay 3% of their assessable profit as tertiary education tax allocated to TETFUND. In addition, the NASENI Act requires the FIRS to collect 0.25% of profit before tax from companies in industries such as banking, telecommunications, ICT, aviation, maritime, and oil & gas, provided their turnover was at least ₦100 million. Companies in sectors like banking, insurance, telecommunications, and ICT with an annual turnover of ₦100 million or more are also charged 1% of profit before tax as an information technology tax, payable annually in favour of the National Information Technology Development Agency (NITDA) Fund. It is also important to note that the number of beneficiaries of earmarked taxes has now grown from three to seven. Initially, the reform committee had recommended drastically reducing the beneficiaries to just one—the Student Education Loan Fund (NELFund). The proposal also included a phase-out plan: allowing the NITDA Fund and NASENI Fund to continue only until the 2026 year of assessment, and the TETFund until 2029. Despite these recommendations, the final act retained all three beneficiaries and added four more, while distributing the new 4% development levy among them as follows: (TETFund – 50%, NELFund – 15%, Defence and Security Fund – 10%, NITDA – 8%, NASENI – 8%, National Cybersecurity Fund – 5%, National Board for Technology Incubation – 4%).

From the Nigeria Tax Act, a 5% surcharge will be applied to the retail price of petrol, diesel, and aviation fuel and will be collected monthly by the NRS. This provision existed under the Federal Roads Maintenance Agency (Amendment) Act of 2007 but was never implemented. As such, its inclusion in the Nigeria Tax Act is said to be about harmonisation rather than immediate implementation. The committee also noted that the surcharge is designed as a dedicated fund for road infrastructure and maintenance and if implemented effectively, it will provide safer travel conditions and reduce travel time and cost. Notably, the proposal in the bill was for the surcharge to be 10% but it was eventually reduced to 5% by the National Assembly.

Similarly, the proposal to apply a 5% surcharge on telecommunication services was scrapped. In a bid to harmonise the taxes in the latest reforms made, the committee initially brought back the 5% surcharge on telecom services (voice and data services), but it was eventually dropped by the National Assembly as well. While various reports have painted different pictures of what this decision means, it is important to clarify that removing the surcharge will not reduce the cost of voice or data services since the duty was never implemented in the first place.

Conclusion

The nature of the political process means that not all proposed changes will scale through. So, the fact that some of provisions and promises didn’t make the final cut does not take anything away from the significance of the tax reform. The fact that some of provisions of the signed laws are less than desirable should be seen in the same light. There is no perfect law. The task is to take valuable lessons from the whole process, make prompt adjustments where needed, and focus on effective implementation.

Expanding the tax net to allow higher income earners pay more tax is a welcome development but for the tax reforms to truly deliver results, the government must embark on a more efficient revenue collection system that can decisively curb tax evasion, particularly among companies and high-net-worth individuals. On expanding the tax net, the gold standard is to combine a wide base with a low rate. Excluding a substantial portion of the tax base flies in the face of this position. There are thus valid concerns about the potential impact on Internally Generated Revenue (IGR) at the subnational level. Pay-As-You-Earn (PAYE) forms nearly half of state governments' total IGR. Outside of commercial cities such as Lagos, Port Harcourt, and the Federal Capital Territory, most states rely heavily on PAYE from middle- and low-income earners. With reduced PIT rates, which will favour low-income earners, many states may face difficulty maintaining their current revenue levels, which will have implication for overall tax revenues.

This brings us to the biggest challenge. Nigeria has set for itself a very ambitious target of raising its tax-to-GDP ratio to at least 18% within the next three years. Achieving this will be no small feat. With lower PIT rates for low and middle-income earners, and no upward adjustment and increased exemptions in VAT, the space for revenue growth has narrowed despite additional surcharges on fuel and solid minerals. For the country to meet this important target, tax administration needs to become more efficient.

[1] https://statehouse.gov.ng/news/mr-presidents-address-at-the-inaugural-meeting-of-the-presidential-committee-on-fiscal-policy-and-tax-returns/

[2] https://ataftax.org/library/african-tax-outlook-2024/

[3] https://www.linkedin.com/pulse/proposed-vat-reform-reduce-increase-inflation-taiwo-oyedele-kxdof/

[4] https://www.pwc.com/ng/en/assets/pdf/how-to-fix-nigeria-broken-vat-system.pdf

[5] https://tribuneonlineng.com/why-we-want-firs-changed-to-nrs-taiwo-oyedele/

[6]https://www.thecable.ng/tax-reform-committee-proposes-slashing-cost-of-collection-to-1-to-improve-efficiency/