- Details

-

By Agora Policy

By Agora Policy - Policy Memo

- Hits: 411

By Odion Omonfoman | The centrality of adequate and reliable electricity supply to individual welfare, economic growth and overall national development cannot be over-emphasised. This message is not lost on Nigeria. However, various initiatives and reforms aimed at creating an optimal power sector for the country have fallen short. The reforms initiated by the President Olusegun Obasanjo administration, leading to the privatisation of the power sector in 2014, is yet to yield the desired results.

According to the World Bank1, Nigeria has the largest energy access deficit in the world. 85 million Nigerians, representing 43% of the country’s population, don’t have access to grid electricity. In comparison, 85% of Ghana’s population have access to electricity, while 70% of Senegal’s population have electricity access2. The World Bank estimates that the lack of reliable power costs the Nigerian economy over $26.2 billion (N10.1 trillion) which is equivalent to about 2% of Nigeria’s GDP.

This is not to say that Nigeria has not made some progress in the power sector since 1999. For instance, in 1999, Nigeria had nine power generating stations—three hydro and six thermal stations—with a total installed on-grid generation capacity of 5,906 MW, but with available generation below 1,500 MW3. Today, Nigeria has up to 26 on-grid generation stations with a total installed capacity above 13,000 MW. However, available generation capacity hovers around 4,000 MW, with average daily energy output of about 100,000 MWH. Sadly, the little progress that has been made in the power sector since 1999 is neither at par with our population growth nor adequate for the energy needs necessary to achieve our economic potential. For reference purposes, Nigeria’s energy consumption per capita at 140kWh is relatively low and is three times lower than the average for Sub-saharan Africa4.

The privatisation of the power sector in 2014 was intended to address Nigeria’s power sector infrastructure and operational challenges, by reducing the direct participation of government in electricity generation and distribution, creating an efficient, contract-driven electricity market, and putting the power sector in the hands of private investors, who would bring capital, operational capacity and efficiency into the sector. Unfortunately, privatisation of the power sector hasn’t really taken government out of direct participation in the sector, nor has it improved operational efficiency in the sector.

As a matter of fact, government’s role and direct participation in the sector has not only expanded, government is currently the largest provider of capital to the sector. Since 2015, government has provided over N4 trillion in capital to the power sector supposedly managed by the private sector. Even worse, the privatisation of the sector has created a huge debt burden for the government, arising from market obligations to private investors. The market obligations were created as liabilities under the balance sheet of the Nigeria Bulk Electricity Trading Plc (NBET), which is a government entity set up to buy wholesale power from electricity generation companies (GenCos) under Power Purchase Agreements (PPAs) and sell same to electricity distribution companies (“DisCos”) under vesting contracts with the DisCos.

The market obligations are mainly debts owed to gas suppliers, shortfall payments to GenCos under the PPAs, and market shortfalls arising from non-review of electricity tariffs by the Nigerian Electricity Regulatory Commission (NERC), the sector regulator. The Federal Government has also gone on a borrowing spree to fund the power sector, particularly the national transmission grid managed by the Transmission Company of Nigeria (TCN), which is still 100% controlled by the government. Some of the loans have been used to fund the improvement of electricity distribution infrastructure of DisCos and also to finance electricity prepayment meters for end-user customers under the National Mass Metering Programme (NMMP).

Policy Recommendations for the Next Administration

Adopt a Paradigm Shift from Installed Capacity to Electricity Consumed

Electricity, however it is generated, is a commodity and has to be consumed (or stored) for electrical energy to be useful. The most meaningful measure of electrical energy in any economy is how much consumption there is. Thus, there is a need for government to stop thinking about electricity in terms of megawatts (MW) that can be generated, and start thinking in in terms of incremental megawatt-hours (MWh) generated and consumed. In other words, government should stop thinking of installed generation capacity and start to think in terms of the amount of electricity delivered, or in layman’s terms, how much electricity is generated and consumed every hour by electricity consumers in Nigeria.

This is an important paradigm shift with positive impact for government, as having such policy mind-set changes the prioritisation and allocation of public and private resources to projects, interventions and initiatives across the electricity value chain that will increase the energy output, availability, reliability and quality of electricity delivered to end-users. By the way, electricity consumers are billed on a kilowatt-hour (kwh) basis (consumption), not on a kilo-watt(capacity) basis.

Under the new paradigm, we expect the incoming administration spokespersons to make statements such as “we will increase the total electricity delivered to Nigerian households and businesses from xyz megawatt-hours (MWh)by 100%within x months”, rather than the usual statement saying “we will increase generation capacity to 20,000 megawatts (MW)”.Increasing generation capacity to 20,000 MW without most of the 20,000 MW being consumed or a corresponding increase in electricity consumption is not only meaningless but also fiscally detrimental to the country.

Increase in megawatt-hours delivered to electricity customers can be achieved if there is a seamless conversion and flow of energy from the natural gas fields to the generation stations, and from the generation stations to the high-voltage lines that transmit the energy to the national grid, and ultimately to medium-voltage and low-voltage lines that distribute the energy to end users. In this regard, the incoming administration needs to prioritise solving the interface issues and challenges across the entire power sector value chain (from natural gas-to-electricity interface, generation-to-transmission interface to transmission-to-distribution interface), building on the current initiatives and projects of the President Muhammadu Buhari government, with a strategic objective to optimise the value-for-money outcomes of a number of these projects, initiatives and interventions.

Continue with Implementation of the Buhari Administration Power Sector Programmes

As stated above, the incoming administration needs to continue the implementation of the power sector programmes, initiatives and interventions carried out by the Buhari Administration. Often times, new administrations are under political pressure to either terminate, suspend, put on hold, or create parallel projects, policies and interventions in the power sector. As an example, the administration of late President Umaru Musa Yar’Adua government suspended indefinitely the implementation of the National Integrated Power Projects (NIPP) and other power sector reform initiatives by the administration of President Obasanjo, with great negative consequences that the power sector is yet to recover from.

The Buhari administration initiated a number of interventions to address the challenges of the power and improve the infrastructure across the sector. The most talked about is the Siemens power projects, being implemented under the Presidential Power Initiative (PPI). The Siemens project is a three-phase infrastructure initiative designed to rehabilitate, upgrade, modernise and expand power transmission and distribution infrastructure across Nigeria. Phase one of the PPI is estimated at 2.3billion euros. 85% of the funding will come from a consortium of German banks and in certain instances, Development Finance Institutions (DFI) at a concessionary rate, and guaranteed by the German Export Credit Agency and other export credit agencies. The Nigerian Government will provide a counterpart funding of 15%. The implementation of the phase has since commenced, with many of the long lead transmission equipment scheduled to arrive before the end of Q2, 2023. The successful implementation of Phase 1 of the PPI will add 2GW of stranded generation capacity to the national grid, and will certainly increase the daily electricity delivered to electricity customers from the present daily average of 100,000 MWH.

Aside from the Siemens projects, the TCN has also secured a number of offshore financing to improve transmission infrastructure across the country. The Central Bank of Nigeria has also been involved in providing long-term capital to the sector for transmission and distribution interface projects. The World Bank funded DISREP is a $500 million programme to help improve service quality of DisCos in the areas of metering, loss reduction and distribution infrastructure network rehabilitation, improvement and expansion. The National Mass Metering Programme (NMMP) is an initiative aimed at closing the metering gap in the country.

The incoming administration should continue the implementation of these and perhaps other projects and initiatives of the Buhari administration in the electricity sector. While we advocate for the continuation of the Buhari administration interventions, the incoming administration should also review and optimise some of these programmes and initiatives to ensure value-for-money.

Develop a New National Electricity Policy Framework & Amend the EPSRA

Nigeria’s subsisting national electricity policy was developed in 2000. The policy has basically remained unchanged since it was developed under late Dr. Olusegun Agagu as the Minister of Power. The National Electric Power Policy was the policy document that guided the power sector reforms and gave birth to the Electric Power Sector Reform Act passed by the National Assembly in 2004 and signed into law by President Obasanjo in 2005. Since its passage, the EPSRA (2005) has also remained unchanged, despite the urgent need for more reforms in the power sector.

With the recent constitutional alteration of section 14(b) of the concurrent legislative schedule of the 1999 Constitution (as amended), it has become more imperative to develop a new national electricity policy. More so as decarbonisation and energy transition from fossil fuels to clean sources of energy are now very important aspects of any country’s national energy policy. Consequently, the incoming administration must develop a national electricity policy that reflects the electricity aspirations of both the Federal Government and the states in line with the new provisions of the Constitution.

In same vein, the EPSRA (2005) is no longer fit-for-purpose. The 9th National Assembly had commenced the process of repealing or amending the EPSRA. While the Senate repealed the EPSRA (2005) and passed the Electricity Bill 2022, the House of Representatives just passed the EPSRA amendment bill in April. It is hoped that the 9th National Assembly can conclude the legislative process of harmonising the two bills, and pass the harmonised bill for presidential assent before May 29th, 2023. However, there is no certainty that this will happen or that President Buhari will sign the bill into law before leaving office.

In the event that the EPSRA repeal/amendment bill is either not passed by the 9th National Assembly, or that President Buhari declines assent to the bill, the incoming administration should fast-track the passage of a new electricity act by the 10th National Assembly to reflect the new electricity frame work as envisaged by the Constitution and give States the unfettered rights to develop the electricity sector, including creating electricity regulatory structures and state electricity markets within their territorial boundaries.

The new electricity law should strengthen the national regulatory framework and the powers of the NERC as the electricity regulator, improve and strengthen existing electricity market structures, incentivise the market to a more efficient, contract-based market, decentralise the operations of the TCN and in general, reduce government’s participation and allow more private investments in the power sector by opening up the sector to greater market competition.

Establish a Standing High-Level Inter-Ministerial Energy Committee

Lack of effective co-ordination of the various segments of the power sector value chain is one of the causes of the dysfunction in the sector. Thus, the incoming government should consider the establishment of a standing inter-ministerial energy committee to be chaired by the Vice President. The inter-ministerial committee members should include the Minister of Power, Minister of Petroleum Resources (or such designate), Minister of Finance, the Permanent Secretaries of the mentioned ministries, the chief executives of NERC, the Nigerian Upstream Petroleum Regulatory Commission (NUPRC) and the Nigerian Midstream and Downstream Petroleum Regulatory Agency (NMDPRA), the Governor of the Central Bank of Nigeria and heads of other key agencies and departments in the oil and gas sectors and the power sector. The inter-ministerial committee’s role will be to ensure effective coordination of agencies and operators that are part of the gas-to-power value chain.

Empower States to Develop Sub-national Electricity Markets

With the constitutional amendments that grant states’ houses of assembly the power to make laws for electricity generation, transmission and distribution within areas covered by the national grid in their domains, states and other sub-national governments have finally become players in the electricity market. The incoming administration should work with the states to develop the electricity markets within their localities.

State governments should be encouraged to take steps to begin to develop the electricity resources within their areas in collaboration with the Federal Government and under the framework of the new national electricity policy and amended EPSRA. That means the incoming state governments will also need to develop the right electricity policy framework for their states, and develop the right legal and regulatory frameworks that would create efficient and competitive electricity market structures, which can help them to attract needed investments into the electricity market. Also, states should be encouraged to drive rural electrification.

Improve the Energy Mix &Address Energy Transition Issues

Nigeria’s energy mix consists of fossil fuel and renewable energy sources, mainly hydropower generation and increasingly generation from solar energy. However, our energy mix is still dominated by fossil fuel—natural gas and diesel/petrol (largely for self-generation). This is understandable as Nigeria has Africa’s largest crude oil and natural gas resources. However, this presents a problem for Nigeria as the world moves to cut fossil fuel consumption in order to achieve carbon neutrality (net zero CO2 emission).

At the United Nations Climate Change Conference event in Glasgow (COP 26), Nigeria committed to carbon neutrality by 2060, and to this effect has unveiled its Energy Transition Plan (ETP). An Energy Transition Implementation Working Group (ETWG), situated in the Office of the Vice President, has been established to drive the implementation of the plan. In the ETP, Nigeria puts forward a robust argument for the utilisation of its vast natural gas resources as a transition fuel for its energy requirements. It is reassuring that the World Bank in a recent publication recognises that natural gas can be a transition clean fuel for developing countries like Nigeria with vast natural gas resources and existing natural gas generation plants.

Consequently, the in-coming administration must continue the implementation of the ETP to achieve a faster transition to carbon neutrality by 2060. There needs to be focused investments at targeting new investments in additional power generation into renewable energy power generation sources such as solar and hydropower energy sources. At the moment, there is no solar energy generation into the national grid – and for obvious reasons ranging from grid connection, grid instability, existing stranded generation and payment assurances for the power to be produced.

However, it is high time that a grid-based, solar energy generation plant is established to optimise our power generation resources and reduce the percentage of fossil fuel in our national energy mix. Beyond having an on-grid solar power plant, there needs to be continued and sustainable investments in off-grid renewable energy generation, such as mini-grids, to serve rural communities and underserved communities. However, this should be done with greater collaboration between the Federal Government agencies responsible for rural electrification and the state governments.

Resolve the Privatisation Puzzle

The privatisation of the power sector is one of the most controversial privatisation exercises so far in Nigeria. A lot has been written about the privatisation but suffice to say that the Eldorado promised with the privatisation of the sector has not yet materialised. Many would blame the Federal Government at the time for forcing through a privatisation of the power sector that clearly was not at the stage to be privatised. But this is neither here nor there. The task is to address whatever gap exists.

This is not to say there has not been any progress in the power sector since privatisation. As a matter of fact, the privatisation of the sector increased total available generation capacity since 2014, as core investors in the successor GenCos invested to rehabilitate and restore installed capacities in some GenCo plants. For instance, the core investors in Egbin, Kainji, Ughelli and Jebba power plants have restored the installed generation capacities for these plants.

At the heart of the seeming failure of the power sector privatisation exercise is the inability of the electricity industry to achieve a contract driven, regulated market as envisaged in the power sector reforms. Only recently, it was reported that the partial activation of contracts in the sector spearheaded by the NERC in June 2022 has collapsed. Without activated contracts (PPAs, Vesting Contracts, Gas Supply Agreements, etc) amongst market participants in the NESI value chain, the benefits of privatisation may never be realised.

Consequently, the incoming administration should prioritise the resolution of the privatisation conundrum, particularly with a view to ensuring a “sensible activation” of contracts in the industry. By “sensible activation” of contracts, we mean allowing more bilateral negotiations, rather than an imposition, of market contracts amongst parties in the industry, under the regulatory oversight of the NERC.

The in-coming administration also needs to look at re-privatising some of the DisCos that have been taken over by lenders due to default by core investors in meeting the acquisition loan repayment terms to the lenders, or under some form of administration by the NERC and the CBN. The failed DisCos in administration should be broken into smaller franchise areas preferably along state boundaries, and privatised as new entities. Lastly, there is the “unspoken” issue of the payment of the huge market debts in the sector. For instance, GenCos claim that they are owed over $1 billion by the NBET. It is unclear how the new government would address the payment of these debts.

Reversing the privatisation of the power sector should not be contemplated under any circumstance. The privatisation process has built-in contract provisions to address the failures of any core investor under their performance agreements. What is needed is for the government to activate these contract provisions, provided the government has also met its own obligations too to core investors.

Improve Gas Supply to the Power Sector

As earlier stated, Nigeria’s energy mix is largely driven by natural gas. Consequently, the unimpeded availability and supply of natural gas to thermal power stations is most critical in attaining incremental megawatt-hours of electricity consumption by end-users, transmission and distribution infrastructure permitting. While Nigeria has the largest natural gas reserves in Africa, our power generation plants engage in a daily struggle to get enough natural gas to run their gas turbines.

Thus, improving gas supply to the power sector will require addressing the bottlenecks in the gas–to-power value chain. These bottlenecks include insufficient investments in gas-to-power infrastructure, and gas-to-power pricing and timely payments to gas suppliers for contracted gas delivered to power plants. From its policy document, the incoming administration plans to introduce a “Nigeria First” policy to prioritise the utilisation of Nigeria’s natural gas resources to electricity generation before export. This will be a welcome policy, if developed and implemented.

However, the issues around gas supply to the power sector are also anchored around sustainable investments in natural gas exploration, development and production. Equally important is robust security and protection of oil and gas infrastructure across the country. Thus, any “Nigeria First” natural gas utilisation policy must seek to address these upstream and downstream issues in the oil and gas sector.

Conclusion

There is a temptation to delve into more tactical issues and challenges in the power sector such as resolving the metering gap, estimated billing, resolution of financial distress in the power sector and other operational issues affecting the electricity industry. Putting together the tactical plan to resolve the issues should be left with the power sector team to be assembled by the incoming administration. Some of the recommendations here can serve as guides to the incoming president in thinking about the critical issues in the sector and in setting the terms of reference for his power team.

[1]https://www.worldbank.org/en/news/press-release/2021/02/05/nigeria-to-improve-electricity-access-and-services-to-citizens

[2] https://ourworldindata.org/energy-access

[3] National Electric Power Policy Document, 2001

- Details

-

By Agora Policy

- Policy Memo

- Hits: 287

By Fola Aina | The Nigerian state is currently confronted with multiple security threats, most of which emanate from, and are perpetuated by violent non-state actors (VNSAs). In the troubled Northeast region, the predominant threats include the activities of violent extremist organisations such as the Boko Haram driven by a political ideology of establishing an Islamic Caliphate, and its first breakaway faction Ansaru, as well as its second breakaway faction, the Islamic State in West Africa Province (ISWAP). The most affected states include Adamawa, Borno, and Yobe states, popularly referred to as ‘BAY’ states. As of 2021, Boko Haram has been responsible for the deaths of 350,000 people,1 and the internal displacement of 2.5million people as of January 2023.2

In the country’s Northwest and Northcentral regions, the activities of armed bandits have devasted local communities. Armed bandits numbering over 30,000 were responsible for the deaths of over 2,600 people3, and the displacement of about 1million others.4 Driven by economic opportunism rather than political ideology, the activities of armed bandits have been mostly manifested through brigandage, theft, kidnappings for ransom, cattle rustling, and sexual violence mostly perpetuated against women and girls. Armed banditry which remains a very significant threat to Nigeria’s national security has its roots in the country’s persistent farmer-herder crisis.

In the Southeast region, secessionist agitations by the Independent People of Biafra (IPOB) and its paramilitary wing, the Eastern Security Network (ESN), have disrupted peace and continues to threaten the freedoms of citizens through the imposition of sit-at-home orders. Added to these are also issues of piracy and terrorism that have plagued the Niger Delta, thereby resulting in the region’s insecurity. In the Southwest region, the activities of cultists, kidnappers and other organised criminal gangs continue to threaten the peace and security of the region as well. These threats have since evolved overtime and adapted making the quest to addressing them even more challenging. This is particularly pertinent as their existence reflects an afront on the state’s monopoly of the use of force.

The degree of severity across these multiple threats varies, given that they have the potential to continually derail social, political, and economic development across the Nigerian state. Collectively, these threats pose significant challenges to human security in Nigeria. These

challenges are mostly manifested in the effects of these threats to human lives and livelihoods. Furthermore, they constitute a grave threat not only to Nigeria’s national security, but also to those of its immediate neighbours such as Cameroun, Chad, and Niger in the Lake Chad Basin region as well as the Sahel region.

Nigeria’s current security architecture is ill-positioned to address these threats. From issues associated with the lack of adequate equipment to those of manpower shortages and non-professionalism, the challenges confronting the security sector abound. This has also contributed towards the proliferation of private security companies (PSCs) in complementing the security provisioning across the country.

Tackling growing insecurity efficiently and effectively will demand reviewing and changing how the security sector is governed in Nigeria. This is in addition to recalibrating the state’s coercive apparatus and repurposing its preparedness and responsiveness to these threats. The Nigerian state has mostly responded to threats to its national security in a reactionary way, rather than proactively.

Repositioning National Security Through Improved Governance

Currently, Nigeria’s national security architecture can be broadly categorised under two sub-headings. These include internal security and external security. Under internal security the state’s institutions mostly saddled with the responsibility of protecting the state from internal threats include the Office of the National Security Adviser (ONSA), the Nigerian Police Force (NPF), the Nigerian Police Intelligence Response Team (IRT), the Department of State Security (DSS), the Federal Ministry of Interior, the Nigerian Customs Service, the Nigerian Immigration Service, the Nigerian Correctional Services, the Nigerian Drug and Law Enforcement Agency (NDLEA), the Defence Intelligence Agency (DIA), the Economic and Financial Crimes Commission (EFCC), and the Independent Corrupt Practices and Other Related Offences Commission (ICPC), and the Nigerian Counter-Terrorism Centre (NCTC), and the Nigerian Financial Intelligence Unit (NFIU), to mention a few. Others at regional levels include Amotekun in the Southwest region, and Ebube Agu in the Southeast region, in addition to local vigilante groups.

With respect to external security, it is pertinent to note that the Office of the National Security Advisor (ONSA) also plays a fundamental role in this regard. Others also include the Nigerian Customs Service and the Nigerian Immigration Service, the Nigerian Intelligence Agency (NIA), the Nigerian Counter-Terrorism Centre (NCTC), the Nigerian Armed Forces (The Nigerian Army, the Nigerian Navy, and the Nigerian Air Force), the Directorate of Military Intelligence, Army Intelligence, Naval Intelligence, Air Force Intelligence, the Defence Intelligence Agency (DIA), and the Regional Intelligence Fusion Unit (RIFU) amongst others. It is equally significant to note that the military is fundamentally the state’s coercive apparatus deployed with the goal of averting external aggression against the Nigerian state, given the NPF’s incapacity to address the country’s multiple threats, the military has since assumed an active role in internal security management as well. As of November 2018, Nigeria has had only 334,000 police officers.5 In addition to being overstretched, as of 2019, Nigeria’s total military forces stood at 223,000 personnel.6

The threats to Nigeria’s national security can be broadly categorised into five dimensions. These include the political dimensions, given that some of these threats are triggered by political issues such as actual or perceived political marginalisation. There is also the socio-economic dimension, which stems from issues such as poverty, inequality, unemployment, and illiteracy amongst others. There is also the environmental dimension which bothers on issues such as climate change resulting in desertification and deforestation, water supply shortages, resulting in conflicts over increasingly scarce natural resources. The fourth dimension is the ethno-religious dimension which reflects tensions resulting in communal clashes. Another very significant dimension is the cyber security related dimension. This dimension is mostly manifested through propaganda, the spread of misinformation, and hacking through malware.

Nigeria’s response to national security threats appears to be overly militaristic. The issue with this is that it has the unintended effect of neglecting “human security” which is required in gaining the support of those affected. This is critical to the exchange of influence between the state and society in the pursuit of mutually-linked security goals and objectives. A viable option towards repositioning Nigeria’s national security architecture would be the adoption of an integrated approach towards national security, one which has “human security” at the centre of it all. This implies a prioritisation of the wellbeing of humans, as members of society, to whom the state is obligated to protect by provisions of the constitution and in accordance with the social contract. The components of this integrated approach to national security entails economic security, social security, food security, housing security, health security, and cultural security. To effectively address national security threats, these components are expected to considered not in isolation, but collectively as a whole.

Recommendations:

To better position Nigeria’s national security architecture to respond more efficiently and effectively to the multiple threats confronting the country, the following are some recommendations:

- The need for a review of the National Security Strategy (NSS) every five years. Nigeria’s approach to national security is essentially derived from the NSS. Given the nature of the new and emerging threats to the country’s territorial integrity, which has resulted in irregular warfare within its shores, the NSS should reviewed every five years to ascertain what works and what does not.

- Establishment of the Office of the Director of National Intelligence (ODNI), not as a separate government agency, but under the Presidency. This is to be patterned after a similar institution in the U.S., which was created in 2005 as part of the responses to the 9/11 terrorist attacks, and designed to ensure integration of national intelligence. In the U.S., both the Director of National Intelligence and the National Security Adviser (NSA) report to the president. As it currently stands in Nigeria, the Office of the National Security Adviser (ONSA) plays the role of a coordinating agency on all matters related to national intelligence. This creates room for underperformance on its fundamental role, which is to advise the President on national security matters. The creation of an ODNI would therefore go a long way in ensuring the harmonisation and coordination of all national intelligence thereby fostering the availability of actionable intelligence in a timely manner. This is in line with what exists in the United States of America (USA), which has both the NSA and the ODNI

- Establishment of two designated portfolios, not as separate agencies, but under the Office of the National Security Adviser (ONSA). The recommended portfolios are: the Deputy National Security Advisor (DNSA) on Africa and Economic Affairs and a Deputy National Security Advisor (DNSA) on Grand Strategy, Counterterrorism, and Intelligence. Both portfolios are needed to deepen and broaden the operations of ONSA.

- There is a need for manpower increase across the Nigerian Police Force and the Nigerian Military to provide much needed surge against criminal activities across the country. The current deficiencies that exist with manpower, amongst Nigeria’s security forces leaves them mostly stretched to the limit thereby impeding their abilities to effectively tackle insecurity.

- There is an urgent need to provide state of the art equipment, advanced weaponry, and technology including combat gears, night vision googles, armed drones, surveillance drones and advanced weapon systems across the security forces. The use of state-of-the-art equipment, advanced weaponry and technology offers an edge to Nigeria’s security forces in the increasingly complex and dynamic sphere of asymmetric warfare.

- Regular trainings for members of the security forces are required to sustain their professionalism, and preparedness to address the issues of insecurity currently confronting the country. This should also be strengthened through foreign security forces assistance with partner countries. Doing so regularly would also help to ensure that Nigeria’s security forces are attuned with the latest doctrines, tactics and operational strategies required to persecute the ongoing multiple internal security operations.

- Nigeria’s structure of intelligence should be repositioned to provide actionable intelligence that informs counterterrorism (CT) and counterinsurgency (COIN) operations across the country. This can be better optimised by prioritising a locally driven strategy towards winning the hearts and minds of local communities.

- There is need to prioritise a human security and people-centred approach over the current militarised approach. This should focus on addressing the underlying root causes and triggers of insecurity such as socio-economic grievances, political marginalisation, ethno-religious tensions and environmental degradation.

*Dr. Aina is an international security expert and an associate fellow of the Royal United Services Institute for Defence and Security Studies (RUSI), London, United Kingdom.

Footnotes

[1] United Nations Development Programme, “Assessing the Impact of the Conflict on Development in North East Nigeria”. Available at https://www.ng.undp.org/content/nigeria/en/home/library/human_development/assessing-the-impact-of-conflict-on-development-in-north-east-ni.html (Accessed June 25, 2021).

[2] International Crisis Group, “Rethinking Resettlement and Return in Nigeria’s North East”, Available at https://www.crisisgroup.org/africa/west-africa/nigeria/b184-rethinking-resettlement-and-return-nigerias-north-east, (January 25, 2023)

[3] Ayandele. Olajumoke., and Goos, Curtis., 2021. Mapping Nigeria’s Security Crisis: Players, Targets and Trends”, Available at: https://acleddata.com/2021/05/20/mapping-nigerias-kidnapping-crisis-players-targets-and-trends/ (Accessed 2nd October 2022)

[4] Hassan, Idayat. and Barnett, James, 2022. ‘Northwest Nigeria’s Bandit Problem: Explaining the Conflict Drivers’. In Centre for Democracy and Development. Available at: https://cddwestafrica.org/wp-content/uploads/2022/04/Conflict-Dynamics-and-Actors-in-Nigerias-Northwest.pdf (Accessed 13 July 2022).

[5] Godwin Comrade Ameh, 2018. “IGP Idris Reveals Number of Police in Nigeria”, Daily Post. Available at: https://dailypost.ng/2018/11/14/igp-idris-reveals-number-police-nigeria/ ( Accessed March 27, 2023).

[6] World Bank, 2023. “Armed Forces personnel, Total”, Available at https://data.worldbank.org/indicator/MS.MIL.TOTL.P1?end=2019&start=2019 (Accessed March 27, 2023).

- Details

-

By Agora Policy

- Policy Memo

- Hits: 785

By Babajide Fowowe and Muhammed Shuaibu | As Nigeria prepares to usher in a new administration, the state of the economy remains a key point of interest. This owes largely to the myriad of economic challenges the country faces, as highlighted in the Agora Policy Report on the economy1. A critical issue that the incoming administration has to grapple with is how to revamp the economy, and quickly.

The key macroeconomic statistics do not paint a rosy picture. The inflation rate rose to 22.04% in March2023. Real GDP growth rate fell from 3.40% in 2021 to 3.1% in 2022. The latest statistics show that 40.1% of Nigerians are poor, while unemployment is 33.28%.Despite favourable global oil market conditions, domestic oil production shocks have dampened oil revenue inflows and have drastically increased the cost of the petrol subsidy, thereby widening Federal Government’s fiscal deficit. This has led to crowding-out of critical spending on social services and infrastructure.

While there are numerous development challenges and actions required at all levels of government, this memo focuses on three key policy actions at the Federal level: fiscal, monetary and trade policies. It is our considered opinion that the incoming administration needs to undertake fast, coordinated macroeconomic policy reforms on these three fronts. These policy actions or economic reforms must be predicated on inclusion, transparency and accountability.

2 Fiscal Policy

2.1 State of Affairs

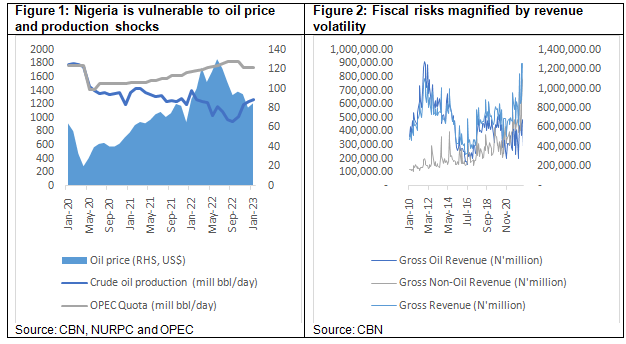

Since the 1970s, Nigeria’s fiscal profile has been tied to the oil sector. Despite the high oil prices in the aftermath of the COVID-19 pandemic, Nigeria’s oil production has been very low. Oil production started falling from 1.799 million barrels per day (bpd) in January 2020 and reached a trough of 937,766 bpd in September 2022 (Figure 1). Since April 2020, the country’s oil production has consistently been below its OPEC quota, and the production shortfall reached a peak of 892,234 bpd in September 2022 (Figure 1). These drastic falls in oil production have come amid a surge in oil prices, with oil prices reaching an all-time high of $130 per barrel in June 2022 (Figure 1). The overall performance of federally-collected revenue has been quite poor, exhibiting heightened volatility in line with global crude oil price movements. FG’s gross oil revenue inflows were N329.984 million in January 2022 but fell to N199.082 million in February 2022. It then started rising and reached a peak of N485.068 million in August 2022 (Figure 2).

The performance of federally-collected gross non-oil revenue exhibited relatively larger swings in 2022. It dropped from N485.645 million in January to N393.012million in March but rose to N805.854 million in July before declining to N616.420 million in September 2022. While the modest improvement could be a reflection of improvements in tax collection, the non-oil revenue generating capacity remains far below its potential especially given the country’s significant spending needs. As pointed out in the Agora Policy report on the economy, many revenue-generating agencies either fail to remit any revenue, or remit a very small fraction to the government. This is a serious problem that needs to be addressed because it deprives the FG of the much-needed revenue. Moreover, the action of such agencies is in violation of the Fiscal Responsibility Act which mandates revenue-generating agencies to remit 80% of their operating surpluses to the Consolidated Revenue Fund and retain 20% in their reserve fund.

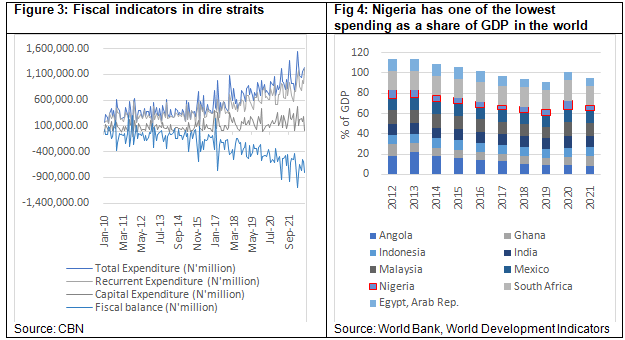

Nigeria’s spending needs have maintained an upward trend since 2010 (Figure 3). However, when compared to other countries, the quantity and quality of spending is low (Figure 4). Figure 3 shows that total FGN spending is largely dominated by recurrent spending with a limited share going to capital expenditure. The average share of monthly recurrent spending in 2021 was about 79% compared with 21% for capital expenditure. Between January and September 2022, average recurrent expenditure was about 84% while capital expenditure was 16%.

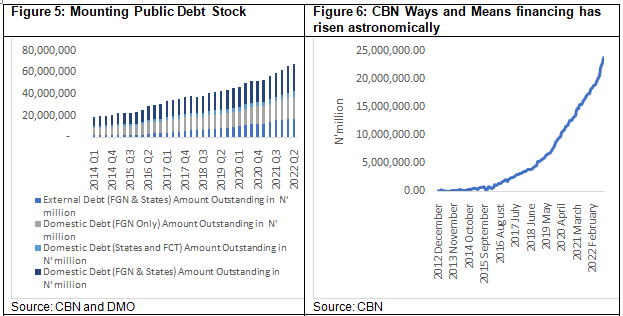

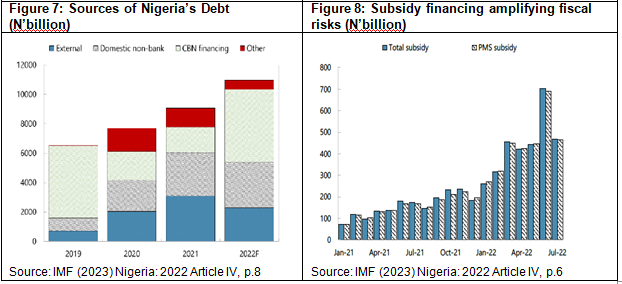

The FG has consistently run a fiscal deficit over the last decade but this has worsened in recent times due to a combination of lower revenue inflows and high fuel subsidy payments (Figure 8). The high fiscal deficit financing need has led to a steady increase in FG’s total public debt stock. FG's domestic debt doubled from N7.18 trillion in Q1 2014 to N14.534 trillion in Q1 2020. Domestic debt further increased to N20.14 trillion in Q1 2022. It is important to note that the official domestic debt statistics does not include ways and means borrowing from the CBN. The Agora policy report on the economy2 highlighted the fact that the FGN’s ways and means borrowing from the CBN had reached N18.8 trillion in March 2022. If this is added to the official domestic debt figures, then total domestic debt would be N38.94 trillion in Q1 2022. The Central Bank of Nigeria’s (CBN) ways and means financing has overshot the statutory limit. Since 2005, FG has increased borrowing through the ways and means financing from CBN (Figure 6). This has been further increased in recent times due to external elevated borrowing costs in the Eurobond market (Figure 7).3

On the external side, the combined outstanding debts of the FG and state governments increased from N8.3 trillion in Q2 2019 to N11.3 trillion in Q2 2020. By Q2 2021, the outstanding external debt stock increased further to N13.7 trillion and rose further to an all-time high of N16.6 trillion in Q2 2022 (Figure 5).

2.2 Immediate Fiscal Reforms

2.2.1 Boosting oil revenue: The drastic fall in oil revenue has been as a result of the double whammy of lower oil production and petrol subsidy. The government needs to take decisive action to address these two critical issues.

Ending oil theft: Addressing the drastic fall in oil production requires urgent action to end oil theft in the oil producing areas. This would require strong determination from the government and crucially, cooperation from host communities and the security agencies. The government needs to review the security architecture in the oil producing areas and give clear instructions about ending oil theft. In addition, both the Nigeria Upstream Petroleum Regulatory Commission (NUPRC) and Nigeria National Petroleum Corporation (NNPC)Limited should be given clear oil production and exporting targets, and be held accountable when these are not met.

Removal of the petrol subsidy: The use of a strategic communication team to engage the public and other critical stakeholders on the benefits and costs of removing the subsidy would be required for the public to buy into this policy measure. At the same time, detailed plans of how funds are saved from subsidy removal need to be extensively discussed and disseminated to the general public to increase trust as a social capital. The savings from the fuel subsidy could be used to scale up short-term direct cash transfers to the poorest and most vulnerable groups in the country. Prices of petroleum products should be market-determined rather that regulated by the government.

2.2.2 Boosting non-oil revenue: There is a need to address the nation’s dismal tax revenue to GDP ratio. The FIRS has done well in recent times by increasing revenue generated from N6.4 trillion in 2021 to N10.1 trillion in 2022, thereby crossing N10 trillion in revenue for the first time. However, for the size of the economy, government revenue and expenditure are grossly inadequate to effectively drive policy, enhance economic growth, lower poverty, and achieve the Sustainable Development Goals (SDGs). This would require two critical actions on boosting non-oil revenue:

Tax reforms and domestic revenue mobilisation: There is an urgent need to broaden the tax net to capture the formal and informal sectors not in the existing tax net. For the formal sector, a first step would be to properly capture and tax high net worth individuals and large corporations. Also, FIRS needs to work closely with the NBS to identify small and medium scale enterprises (SMEs) and ensure they pay taxes appropriately. Some simple incentives and an amnesty period, following which appropriate sanctions will be meted out, can be given to ensure quick compliance. It would be crucial to continuously communicate the issue of tax reforms to the citizens to gain public confidence in the system. In addition, leakages from taxes collected by non-state actors need to be eliminated.

Full compliance with the Fiscal Responsibility Act: The Fiscal Responsibility Act mandates revenue generating agencies to remit 80% of their operating surpluses to the Consolidated Revenue Fund and retain 20% in their reserve fund. There are many revenue-generating agencies that either fail to remit any revenue or remit a very small fraction to the government. The Fiscal Responsibility Act should be amended to set strict penalties for agencies that fail to remit their stipulated operating surpluses. Also, there is the need to stop funding revenue-generating agencies from the federal budget.

2.2.3 Improving the budget implementation framework. This entails strengthening the zero-based budgeting framework by ensuring that budget preparation starts on time. There is an urgent need to end “drip-feeding” which has inhibited the completion of critical capital projects and perpetuated the “ongoing project” syndrome. This comes at zero cost to the key agencies such as the Federal Ministry of Finance, Budget and National Planning and the Budget Office of the Federation. Increased budgetary provisions should be given to capital expenditure. There is also the need to increase the percentage of the budget that goes to capital expenditure and the necessity of trimming recurrent expenditure.

3 Monetary Policy

3.1 Monetary Policy Developments

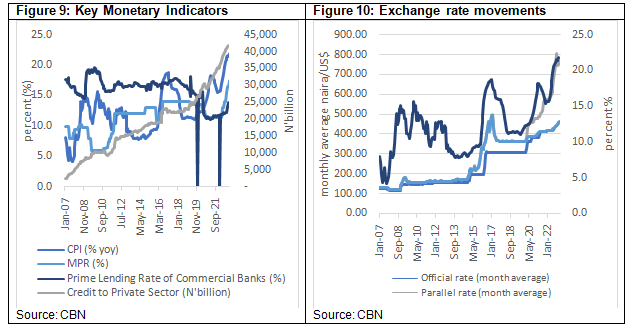

Similar to other central banks around the world, the Central Bank of Nigeria (CBN) has tightened its monetary policy stance to tame rising inflation. The CBN raised the monetary policy rate by a cumulative 5% in 2022 and also increased the cash reserve ratio from 27.5% to 32.5%. Despite these tightening measures, the monetisation of the fiscal deficit and other quasi-fiscal activities such as the intervention programmes have expanded the growth of credit and thus contributed to inflationary pressures. The year-on-year composite price index (CPI) increased from 15.6% in January to 18.6% in June and to 20.8% in September 2022. It moderated marginally to 21.3% in December 2022 before rising again to 21.91% in February 2023. The obvious disconnect between fiscal and monetary policy has heightened macroeconomic risks and vulnerabilities. The weak transmission mechanism of monetary policy is a combination of poor policy coordination and focus of the CBN on economic growth rather than on inflation(Figure 9).

Exchange rate management has remained at the front burner of policy discussions. This is due to the complete exchange rate pass-through to domestic prices in Nigeria. Nigeria currently operates several exchange rate windows, often at varying rates (Figure 10). This has created arbitrage opportunities for speculators in the foreign exchange market. The official exchange rate was N416/$ in March 2022 and had increased to N461/$ in February 2023 (Figure 10). The parallel market exchange rate has continued to diverge from the official rate. In January 2022, the parallel market exchange rate was about N570/$ and had increased to about N761/$ in February 2023. The CBN also created an Investors and Exporters Foreign Exchange (IEFX) window to give genuine importers and exporters access to foreign exchange. This IEFX rate closely mirrors the official exchange rate but is still below the market-based parallel exchange rate. The average IEFX rate in 2022 was about N428/$ and it had increased to N461/$ in January 2023.

- Immediate Monetary Reforms

- Enhance the coordination of fiscal and monetary policy to reduce frictions and counteractive policy goals. The government should strengthen the Fiscal-Monetary Coordination Committee to ensure that the monetary authority (CBN) and the fiscal authority (Federal Ministry of Finance, Budget and National Planning) optimally coordinate policies to ensure the gains from fiscal and monetary reforms are maximized.

- Restore monetary policy focus back to its price stability mandate, taming inflationary pressure and strengthening the monetary transmission. The CBN should focus on its core mandate of maintaining price stability. The CBN should set clear and realistic targets for inflation, and a timeline for achieving these targets. Addressing supply-side bottlenecks such as trade restrictions on critical intermediates that increase the cost of doing business. The CBN will have to restore the credibility of the MPR such that bond yields and lending rates are reflective of the monetary policy rate (MPR).

3.2.3 The removal of the current multiple exchange rate windows being operated by the CBN. This would make the exchange rate market-determined and mitigate speculative pressures that fuel arbitrage conditions in the market. This would further inspire confidence from domestic and foreign investors.

3.2.4 Putting an end to ways and means financing of FGN expenditure. This would curtail the growth of the money supply and thus curtail inflationary pressure. Part of this will involve the CBN helping the FG to properly forecast its revenue as well as helping the FG, on a technical level, identify potential sources of revenue. A strategy will also need to be developed to manage the current stock of FG’s debt at the CBN.

4 Trade and Investment

4.1 State of Trade and Investment

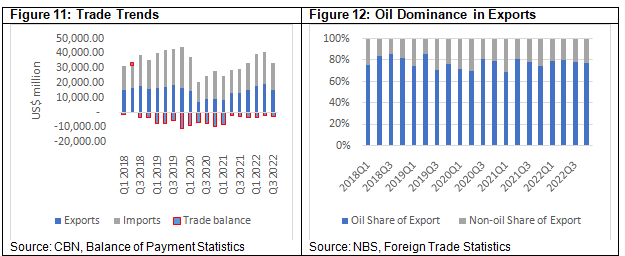

Nigeria has one of the largest economies in Africa, with a significant trade volume. However, the country’s trade profile has historically been dominated by oil exports, which account for a large share of the country’s foreign exchange earnings (Figure 12). The low level of trade diversity and the need to reduce over-reliance on oil exports in Nigeria has remained a major concern for governments over time. Figure 11 indicates that since Q1 2020, with the exception of Q2 2021, Q2 2022 and Q4 2022, imports have exceeded exports, resulting in trade deficits for most of the period.

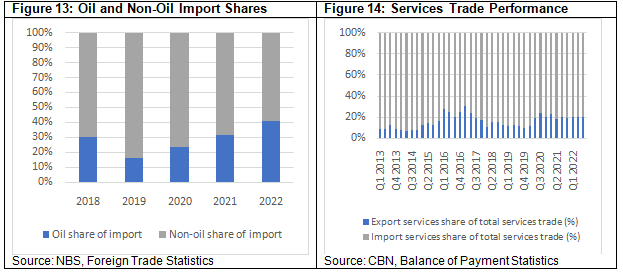

While Nigeria’s export shave largely been dominated by oil exports, the trend of imports depicts a different picture. Non-oil commodities dominate Nigeria’s total imports as they increased from 70% in 2018 to 84% in 2019 and 77% in 2020, before falling to 69% in 2021 to 59% in 2022 (Figure 13).In terms of trade in services, Nigeria’s performance is quite limited as services import dwarfs services export (Figure 14). The average services import in 2018 was about 87% and increased to 89% in 2019 then dropped to 81% in 2020. By 2021, it dropped marginally to 80% and remained at the same average level in the first three quarters of 2022.

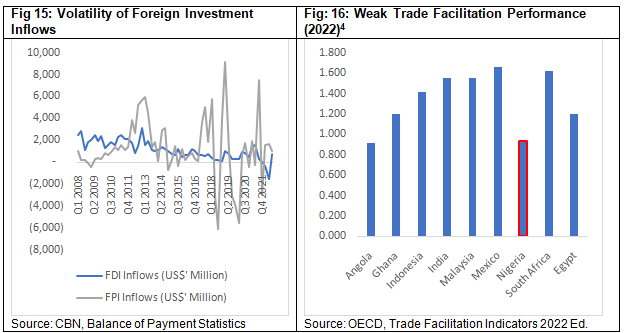

The volatility of capital inflows has persisted over the last decade. FPI inflows in the fourth quarter of 2018 was US$3,935 million but dropped significantly, translating to an outflow of US$3,788 million in the fourth quarter of 2019. By the fourth quarter of 2020, FPI outflow slowed down to US$477 million and even recorded significant improvements with inflows of US$1,926 million recorded in Q1 2021, before dropping to outflows of US$3,012 million in 2021Q4. FPI remained positive in the first three quarters of 2022 recording a drop from US1,542 million in 2022Q1 to US$1,001 million in 2022Q3. In terms of FDI inflows, the fluctuations have been relatively lower than FPI as it rose from US$59 million in 2018Q4 to US$248 million in 2019Q4and US$439 million in 2020Q4. This positive trend reversed by the fourth quarter of 2021 as FDI inflows dropped significantly to US$42 million and for the first time in over a decade recorded an outflow in 2022Q1 (US$323 million) and 2022Q2 (US$1,537 million) before a positive rebound of US$726 in the third quarter of 2022.

One of the major issues that have impeded trade performance and thus diversification in Nigeria is the weak trade-related infrastructure. Having in efficient or inadequate systems of transportation, logistics, and trade-related infrastructure can severely impede a country’s ability to compete on a global scale.5 Based on the 2022 OECD trade facilitation performance indicator, Nigeria performs poorly (0.930) relative to regional peers such as Ghana (1.200), South Africa (1.625), and Egypt (1.200). The trade facilitation performance indicator is composed of a set of variables measuring the extent to which countries have introduced and implemented trade facilitation measures in absolute terms, but also their performance relative to others. The indicator takes values from 0 to 2, where 2 indicates the best performance that can be achieved.6

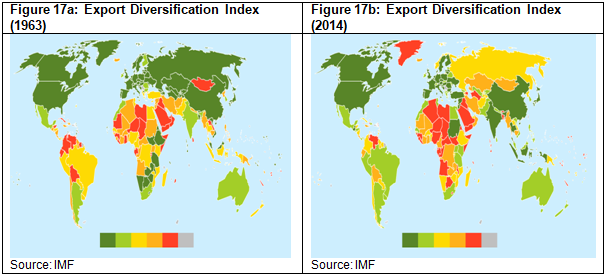

The lopsided structure of Nigeria’s trade performance over time is linked to low trade diversity. Although this has remained at the forefront of various development policy plans, weak implementation and poorly coordinated macroeconomic policy and structural reforms have constrained trade diversification. For example, Nigeria has used several trade restrictions mainly to protect domestic industries and spur domestic productivity. However, this has not achieved the planned objectives as domestic firms remain largely uncompetitive due to structural rigidities tied to the inadequate soft and hard infrastructure. Comparatively, as shown in Figures 17a and 17b, Nigeria’s export diversification has worsened over the last five decades. At 3.74 in 1963, it increased to 4.65 in 1970 and 6.15 in 1980. By 1990 it had reduced marginally to 5.99 before rising to 6.04 in 2000 and then dropping again to 5.54 in 2010. In 2014 Nigeria’s export diversification index was 5.62 which was far below the performance of other countries like South Africa (2.59), Egypt (2.65), India (2.16), Indonesia (2.21) and Mexico (2.43).7It is important to note that higher values correspond to lower export diversification while lower values correspond to high export diversity.

4.2 Immediate Trade and Investment Reforms

4.2.1 Replacement of import bans with import duties. The use of tariffs rather than the existing import bans would spur the domestic productivity of firms, especially those that rely on the import of intermediates that are affected by the import prohibition. This has to be done in a coordinated manner between the Ministry of Industry, Trade and Investment, Ministry of Finance, Budget and National Planning, and the Nigeria Customs Service.

4.2.2 Development of regional industrial hubs and transport infrastructure through PPP arrangements. FGN should prioritise the development of industrial hubs and export processing zones as well as the delivery on critical infrastructure which support international trade, such as ports, roads, and telecommunications networks. In view of obvious budgetary constraints and current revenue shortfalls, the government should seek partnership with the private sector. This could help enhance efficient service delivery and reduce trade costs, thereby making it easy for domestic firms to integrate in domestic and regional value chains.

4.2.3 Reopening all closed borders and removing all food trade restrictions. These have hurt prices and have not led to the expected increase in domestic productivity. The government needs to prioritise the development of a goods and services export strategy in collaboration with the subnational governments. Such a strategy should focus on labour intensive sectors, and should clearly identify priority sectors and potential markets by leveraging Nigeria’s global network of diaspora and consulates.

4.2.4 Creating a conducive environment for attracting foreign investment. The rise in foreign investment outflows needs to be addressed by sending positive signals to foreign investors. The exchange rate needs to be market-determined. Also, security, banditry, kidnapping and insurgency need to be adequately tackled to send positive signals.

4.2.5 Providing incentives for export-oriented firms especially in the non-oil sectors. In order to leverage on the enormous market opportunities created by the African Continental Free Trade Area (AfCFTA) agreement, there should be a gradual reduction of import tariffs on intermediate products used by domestic firms that export or plan to do so. At the same time, the discretionary import duty waiver allocation system needs to be replaced with a clearly defined industry-wide incentive system that supports export-oriented firms.

Conclusion

The Nigerian economy has significant potential but faces several challenges. Nigeria is the largest economy in Africa, with a large and growing population, abundant natural resources, and a strategic location. However, the country has struggled with economic diversification and over-reliance on oil exports, which has made it vulnerable to external shocks. The country also grapples with some structural challenges, including poor infrastructure, limited access to credit, and weak institutions. These issues have hindered economic growth and made it difficult for businesses to thrive in the country. This note highlights some of the key challenges facing the Nigerian economy in the context of fiscal, monetary and exchange rate management, trade and investment policies. It also prescribes urgent actions on those three critical fronts.

*Professor Fowowe and Dr. Shuaibu teach Economics at the University of Ibadan and the University of Abuja respectively.

[1]https://agorapolicy.org/wp-content/uploads/2022/10/Updated-Digital-Version.pdf

[2] https://agorapolicy.org/wp-content/uploads/2022/10/Updated-Digital-Version.pdf

[4]http://compareyourcountry.org/trade-facilitation/en/0/default/all/default/2022

[5]https://www.worldbank.org/en/topic/trade-facilitation-and-logistics

[7]https://data.imf.org/?sk=A093DF7D-E0B8-4913-80E0-A07CF90B44DB

- Details

-

By Agora Policy

- Policy Memo

- Hits: 261

By Adebayo Ahmed | Jobs are one of the foundations for a stable society and key to improvements in quality of life. Unfortunately, unemployment is one of Nigeria’s major challenges today. Beyond the negative impact on human welfare, unemployment is gravely implicated in Nigeria’s other pressing challenges, especially low productivity, poverty and insecurity. It needs to be tackled aggressively and comprehensively, not in the current tokenistic and uncoordinated fashion.

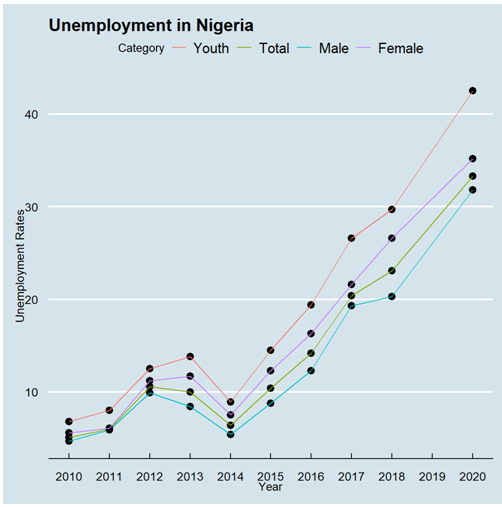

Fig 1: Unemployment Rates. Source: NBS

In the last decade Nigeria has struggled to create enough jobs to meet up with the constant flow of people entering working age. Since 2010 the unemployment rate has been on an upward trajectory rising from 5.1% in 2010 to the last pre-covid estimate of 23.1% in 2018, with the situation worse for women. Unemployment rate rose to 33.3% during COVID, combined with a much-reduced labour force participation rate. There has been little official information since. Although the National Bureau of Statistics (NBS) claims to be working on an improved methodology for measuring unemployment, all we can say at this point is that unemployment is likely still high and at an undesirable level. The situation has been particularly worse for young people who, as at 2020, faced an unemployment rate of over 40%. There is little doubt that this rising unemployment is linked to increasing restfulness and disenchantment among the youth.

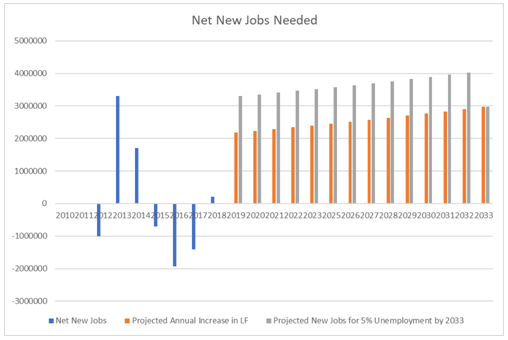

Fig 2: Net new jobs created and needed. Source: NBS, Author’s Calculations.

Given that the population, and hence the labour force, keeps growing, the challenge of reducing unemployment is therefore all about creating more new jobs than there are people entering the labour force. At the very least, to keep unemployment from rising, enough net new jobs need to be created to at least employ the majority of net new entrants to the labour market. What does this mean in the Nigerian context? Based on a labour force of about 90 million1 prior to COVID in 2018, about 2.5 million net new people enter the labour force every year. Which means the economy would have to create at least 2.5 million new jobs a year on average just to keep the number of the unemployed from rising. If we wanted to get the unemployment rate to a healthier five percent by 2033, and we assumed that the labour force grew at the same rate as population growth, then by our calculations, we would need to be creating at least 3.6 million net new jobs a year2. Given that between 2010 and 2018 we only created on average 21,757 net new full-time jobs a year then you can see clearly that we have a problem3. In fact, as shown in Figure 2, 2013 is the only year in the last decade when we actually produced over three million net new jobs.

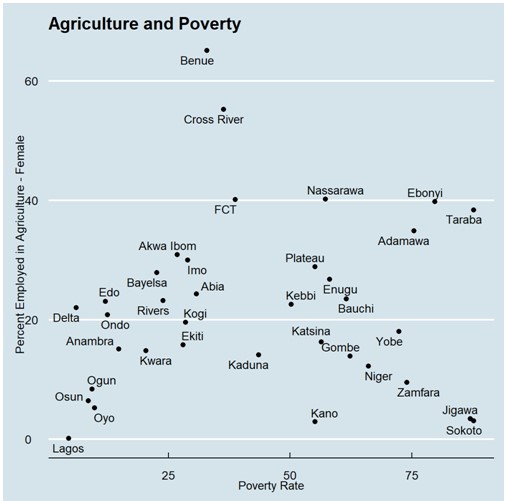

Fig 3: Employment in Agriculture vs Poverty Rates across states (Male and Female).

Source: NBS Living Standards Survey 2018.

If we add the caveat that the jobs created have to be good enough to allow people have a meaningful quality of life, then the challenge is even more difficult. One of the features of current employment, especially in subsistence agriculture, is that some of the jobs do not result in enough income to actually lift the employed persons out of poverty. As observed in Figure 3 above, some of the states with the largest employment in agriculture also happen to be the states with the highest poverty rates. Many of these people are employed but are still living in poverty despite their employment. For example, although Sokoto State had an unemployment rate of 14.3% in 20184, majority of the people were employed in (presumably) subsistence agriculture (51% of males and 3% of females). The implication being that over 87% of households were still living in poverty. In essence, it is not just jobs that are needed but decent jobs.

Limits of current approaches

The current approaches by government to tackling unemployment, while sometimes having merit, have failed to resolve the problem. This is largely because the majority of the approaches cannot reach the scale of what is required.

The first of the common approaches is direct government employment. This is particularly popular at the state and local government level, even if the Federal Government is not left out. Although it is easy to argue that the country needs more police personnel, more doctors, and more teachers, it is clear that government employment alone cannot solve the unemployment challenge. It is almost unfathomable to imagine the federal, state, and local governments combined being able to employ anywhere close to three million workers each year. This is even before you take into account their financial constraints. In fact, according to some reports, the entire Federal Government only employed about 720,000 people as at 20205. The ILO estimates that there were only about 2.12 million people employed in the public sector in Nigeria in 2020. Given the scale of the challenge, it is unsurprising that government employment has not worked in resolving the challenges.

Fig 4: Q3 2018 Unemployment by Educational Category. Source: NBS

A second common approach is the skills-acquisition driven approach. The summary of this approach is that if you teach people some skills, such as carpentry or tailoring, then that should automatically result in employment. For instance, a cursory look at the activities of the National Directorate of Employment (NDE) shows that most of its programmes are essentially skills acquisition programmes. However, unfortunately, in reality skills do not necessarily mean jobs. For instance, in 2018 the unemployment rate for people with post-secondary education at 29.8% was higher than for people with no education at 21.8%. Similarly, as is clear in Figure 4

above, people with only primary education had a lower unemployment rate than people with NCE/OND/Nursing certificates even though they presumably have more skills. Although there are issues such as skills mismatch and selectivity in employment, and there is still significant room for certification for specific skills, it does signify that more skills alone will not necessarily solve the unemployment challenge.

The third, and more recent approach is that of social investment or social transfers as signified by the expansion of programmes such as trader-moni or other direct cash support schemes popular at state and local government level. As with the case with direct government employment, the scale of the challenge means that this is unlikely to be a sustainable approach. According to the NBS6, only between 10,000 and 20,000 thousand were enrolled in the governments N-Power programme in each state as at 2018. The FG stated that it planned to raise the total number of beneficiaries to one million in 2020. The GEEP programmes have similar statistics. Although you can argue about the merits or demerits of such programmes, what is clear is they are not creating, and probably cannot create, the 3.6 million net new jobs a year to tackle Nigeria’s unemployment challenge.

Prescriptions / Recommendations

In thinking of a coherent strategy to tackle the unemployment challenge, we need to take a step back and understand what exactly jobs are. Jobs are essentially the contribution of individuals to economic activity. Which means if you want to see faster job growth then you must have faster economic growth. However, as we learned during the growth episodes in Nigeria in the early 2000s, growth alone does not imply jobs. There can be jobless growth and job-led growth. Specifically, what we need is growth in labour-intensive sectors.

For instance, growth in petrochemical refining or car assembly is unlikely to provide as much jobs per unit of output compared to growth in the more labour-intensive textiles sector. Even within the textile value chain, growth in the relatively capital-intensive part of the chain that converts cotton into fabric, is unlikely to create as many jobs per unit of output as the more labour-intensive part that converts fabrics into clothing. There needs to be a specific focus on engineering sustainable growth in these labour-intensive segments of various value chains. Given the scale required—3.6 million net new jobs a year—the output of this engineered growth will likely need to be targeted at markets much larger than Nigeria’s.

In summary, on a macro level the most likely path to job creation in Nigeria at the scale required, is to engineer growth in labour-intensive portions of value chains for export to large markets. What does this mean in terms of specific policy actions?

From a broader economy-wide perspective, it means:

- Resolving broader macro-economic challenges that limit growth across the board. This includes resolving the dysfunction of multiple rates in the foreign exchange market, and re-focusing the Central Bank of Nigeria (CBN) on its mandate of keeping inflation at optimal levels.

- Targeted infrastructure spending in particular areas that increase the competitiveness of Nigeria’s exports. This would include electricity, transport, and telecommunications investments in export processing zones. For instance, India’s new foreign trade policy 20237 designated four “towns of export excellence” that will get priority access to export schemes and investments.

- Developing and implementing an export-driven trade policy for labour-intensive value addition for export sectors. This could include fast-tracking implementation modalities for participating in the African Continental Free Trade Agreement (AfCFTA), fast-tracking trade agreements that grant Nigerian export access into large markets, and reducing tariffs completely or introducing transparent reimbursement schemes for imports of intermediary goods for value addition.

- Developing a strategy to utilise our large diaspora network as well as our network of embassies and consulates to get Nigerian products into markets around the world.

- Re-organising our technical and non-academic learning protocols to improve on specific skills in areas critical for improvements in competitiveness of targeted sectors. This could include trade schools aimed at providing necessary skills for particular sectors. For instance, if the garment sector is a targeted sector it would include starting up or improving on technical schools and certification for fabric cutting or clothing design software.

- Developing and implementing a strategy to reduce the costs of logistics, both financial and non-financial. This could include things like “trusted firm” schemes that allow customs and security procedures take place inland, at dry-land ports for instance, to by-pass time-consuming procedures at official ports.

- Investing in certification and export processes training in partnership with targeted destination countries to ease the cost of accessing external markets, specifically for SMEs that do not have the financial clout to do this on their own. As has been argued by some economists, SMEs tend to employ more people per output produced. Hence, ensuring SMEs participate in an export push can amplify the scale of job creation.

To improve the decency and capacity of agriculture jobs to provide a minimum income and quality of life, this will mean:

- Developing and implementing a productivity growth strategy for agriculture that will target improvement in yields for subsistence farmers. This will include strategies for improved seed varieties, improved crop choice, irrigation infrastructure, crop-specific weather and market information, crop insurance and social protection etc..

- Developing and implementing a market development and financial innovation strategy for agriculture to ensure that crops have access to markets and off-takers, and predictable and flexible revenue streams.

Finally, to take advantage of the growing global trends in remote work especially in ICT and other export services, this will mean:

- Fast tracking the implementation of the broadband plan to improve the competitiveness of Nigeria’s remote workers.

- Developing a fair, transparent, and competitive taxation policy for remote workers that reduces their incentives to emigrate to tax havens and that incentivizes other skilled workers to opt for Nigeria.

- Working with states to develop livable safe spaces that incentivize skilled workers to remain in Nigeria.

Conclusion

The size of the Nigerian population and the scale of the unemployment challenge implies that piecemeal and uncoordinated approaches are unlikely to make a significant impact. If Nigeria desires to get unemployment down to 5% by 2033, it needs to create 3.6 million jobs a year. To achieve this, it needs a scalable strategy. Given that jobs are simply part of the process of generating economic activity, then Nigeria needs to engineer growth in labour-intensive sectors in general, and labour-intensive parts of value chains in particular.

[1] National Bureau of Statistics Labour Force Survey Q3 2018

[2] A labour force growth rate of 2.41% implies that by 2033 the labour force would have about 126m people. This means to have 5% unemployment then about 120m people need to be employed. Which in turn implies that between 2018 and 2033, about 54m new jobs need to be created. This amounts to about 3.6m net new jobs a year on average.

[3] National Bureau of Statistics Labour Force Surveys 2010 - 2018

[4] NBS – Q3 2018 Unemployment by States

[5]https://leadership.ng/ippis-fg-trims-civil-servants-to-720000/

[6] NBS 2020 Social Statistics in Nigeria

[7] https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1912572

Subcategories

Policy Insight

Policy Insight

![]()

Agora Policy is a Nigerian think tank and non-profit committed to finding practical solutions to urgent national challenges.