By Wale Thompson | The 2023–24 foreign exchange reforms restored market logic, but the present FX market stability remains a function of high-interest-rate 'rent' rather than structural improvements. Without a shift toward earned stability, Nigeria remains one global shock away from a reversal of recent gains.

In May 2023, President Bola Ahmed Tinubu took office with an economy burdened by three interlocking distortions: a costly petrol subsidy, an overvalued exchange rate, and a central bank drawn too deeply into fiscal financing and quasi-fiscal intervention. Those distortions helped mask underlying macroeconomic pressure for a time, but they also weakened public finances, undermined confidence and hollowed out the formal foreign-exchange market. As such, the initial corrective steps by President Tinubu — subsidy removal, exchange-rate liberalisation and tighter monetary policy — were painful, but they were difficult to avoid.

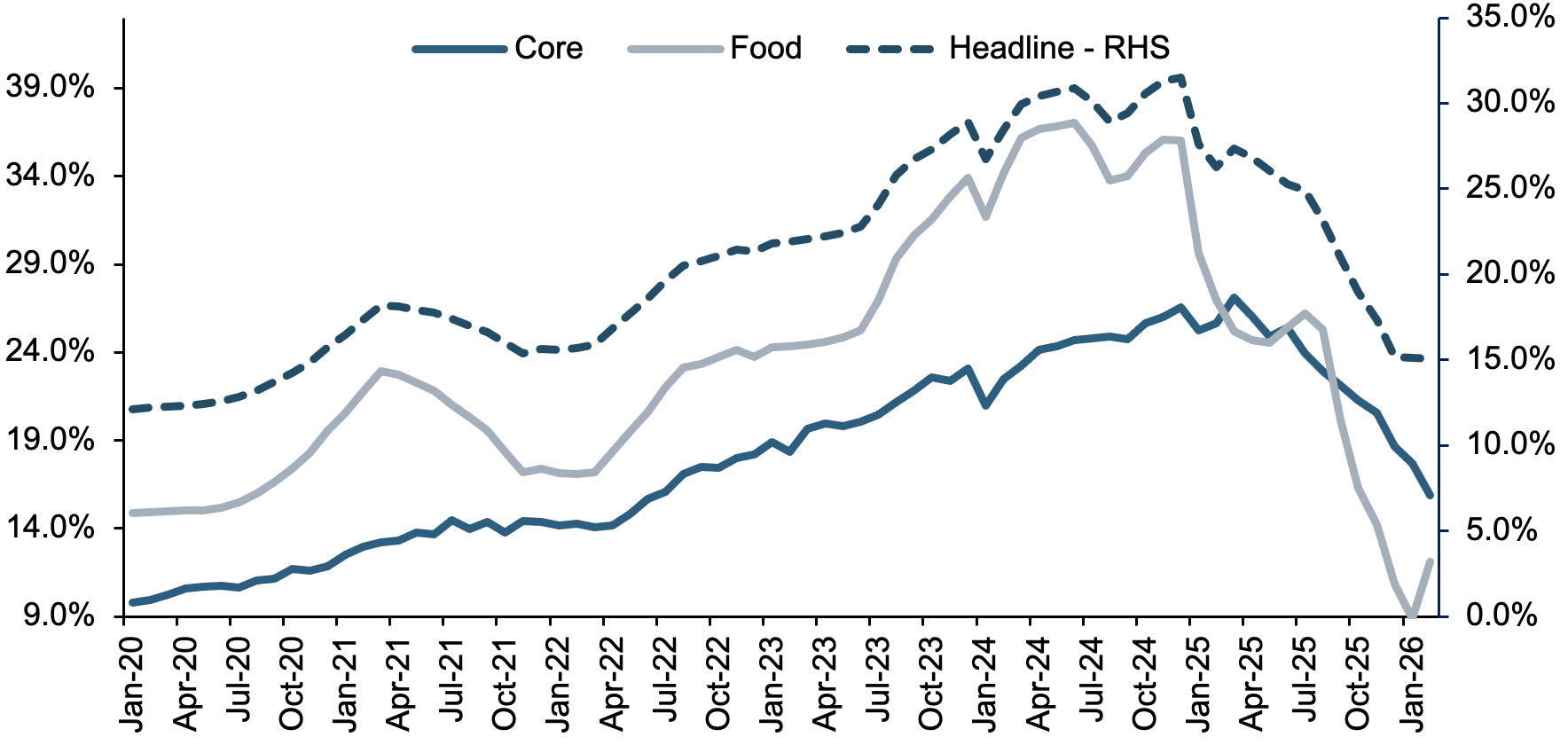

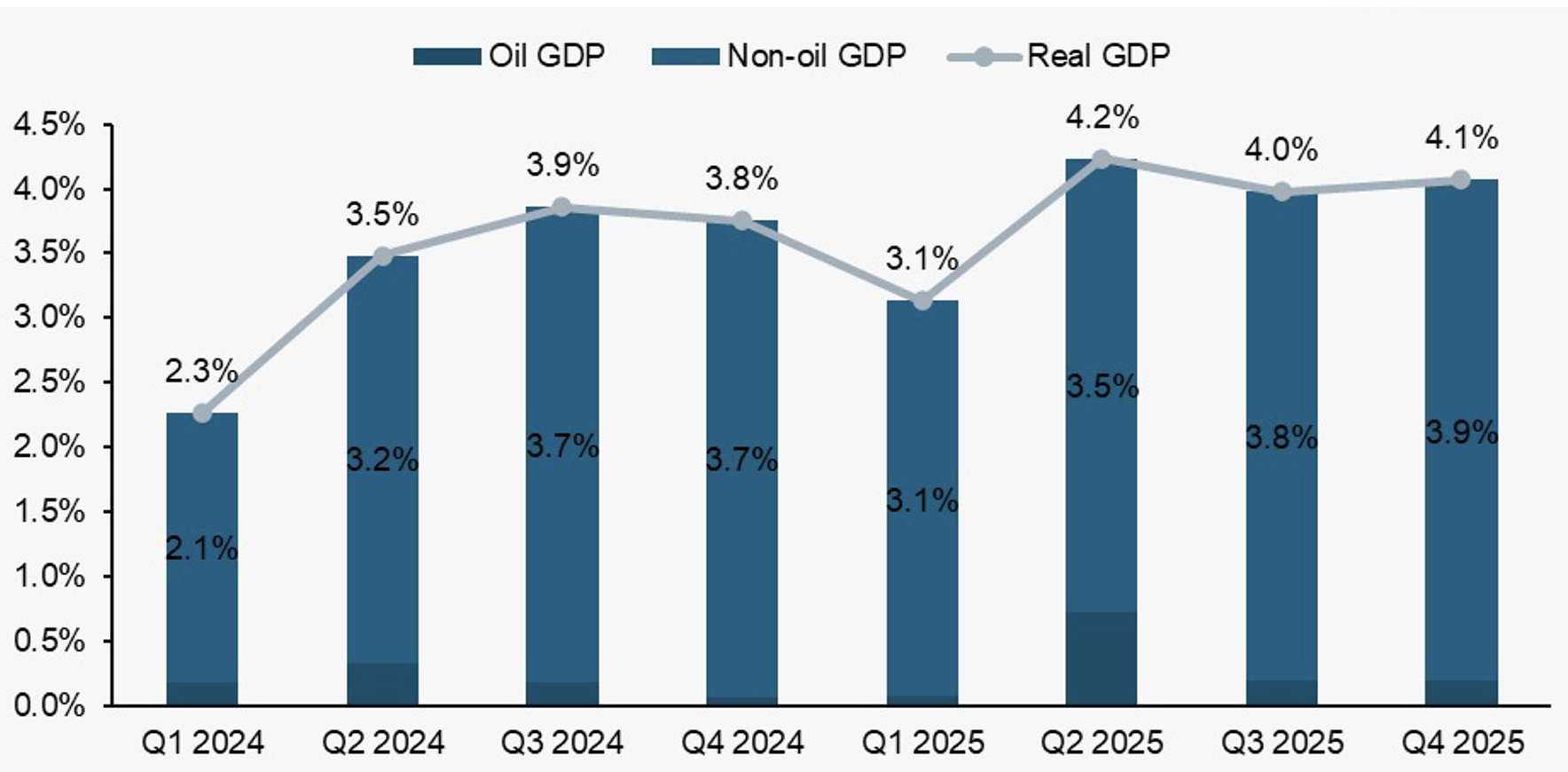

About three years later, some gains from these policy adjustments are visible. Headline inflation has fallen sharply from its 2024 peak, growth has improved, the Naira is no longer as obviously overvalued as it was before the adjustment, and the official FX market is more orderly than it was under the old regime of multiple windows and administrative rationing. In that sense, the first phase of reform achieved something important: it restored price discovery, meaning the exchange rate is now set more credibly by supply and demand than by administrative fiat.

But restoring FX price discovery is not the same thing as building a deep and durable FX market. Much of Nigeria’s recent currency stability has been supported by foreign portfolio inflows attracted by very high domestic interest rates. That can help during an adjustment phase, but it is not a stable long-term foundation. As inflation eases and global markets become more volatile, the yield premium that draws in those flows can narrow quickly, and money that arrived fast can also leave fast. The real test of the next phase of reform is whether Nigeria can move from rented FX stability to earned FX stability. This paper sets out the areas where policymakers must go further if the current reform effort is to endure.

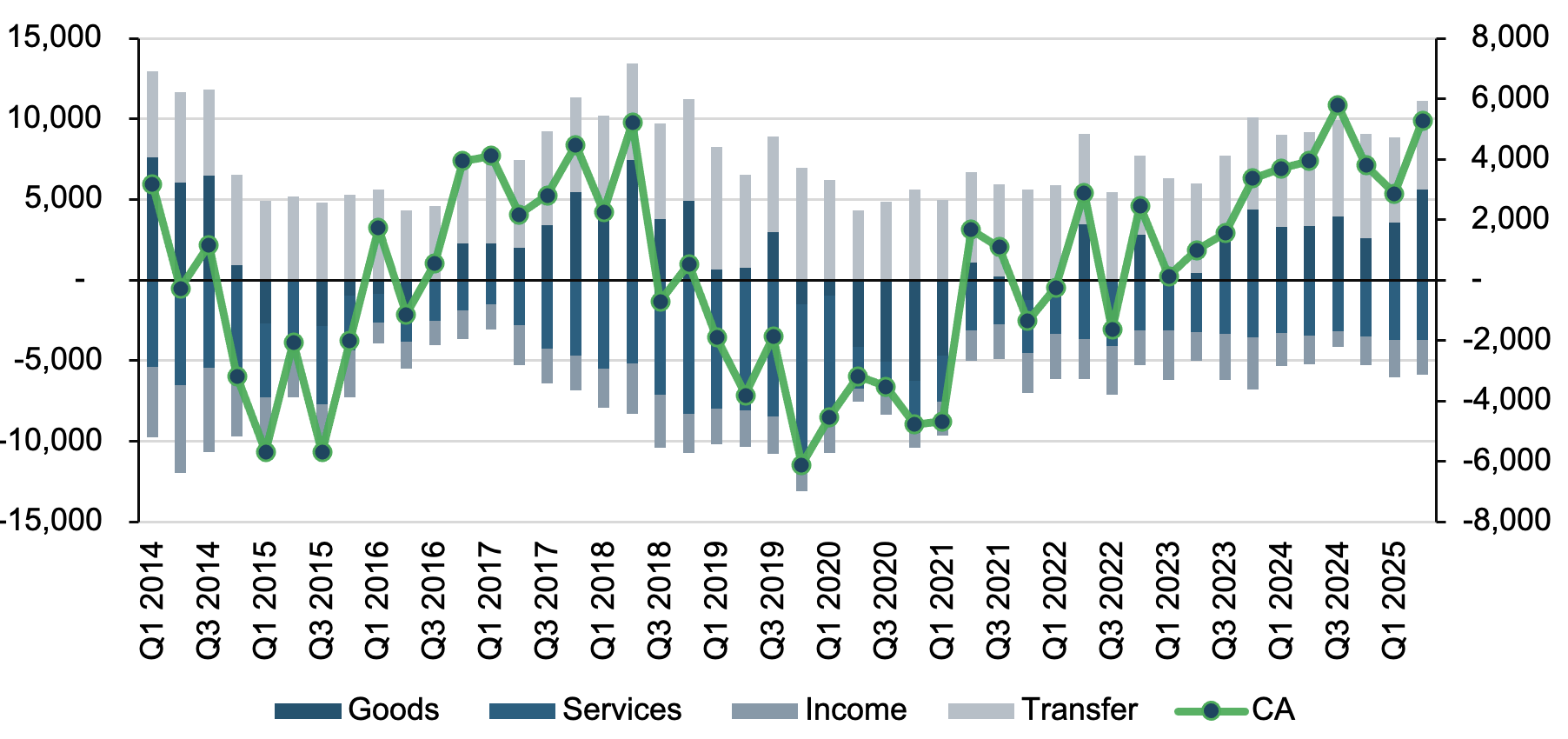

Figure 1: Current Account Balance (USD’ mn)

Source: CBN

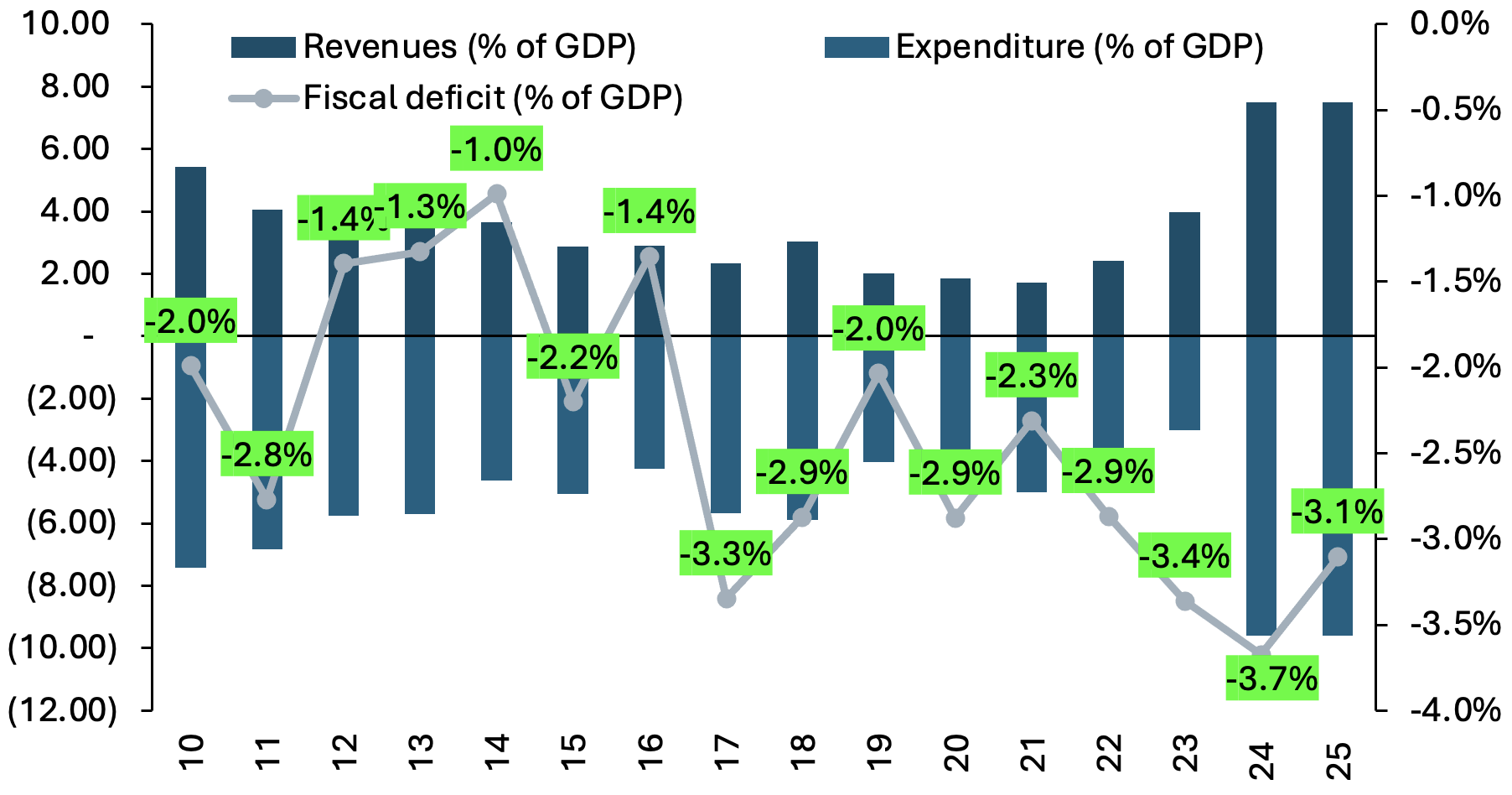

Figure 2: Fiscal Account Balances

Source: CBN

Figure 3: Trends in Headline, Food & Core Inflation

Source: NBS

Figure 4: Trends in GDP

Source: NBS

Moving from Price Discovery to Structural Credibility

Naira’s trajectory since the 2023–24 reform reset has been broadly encouraging. After two years of large depreciations, the Naira appreciated approximately 7% in nominal terms over 2025 and had continued to strengthen into early 2026 before the volatility triggered by the US/Israel–Iran conflict. The Bruegel REER data through February 2026 show that the currency has moved from a position of substantial overvaluation before the reform to a markedly more competitive level in 2024, before recovering materially through 2025. That is an important milestone: it means the Naira is no longer obviously overvalued. But it is equally important to recognise what that benchmark does not mean. The 2000–2014 average was itself associated with recurring crises, periodic capital flight, and chronic FX shortages. Being at that average is a floor, not a ceiling.

Figure 5: Monthly NGN Exchange Rates (Real and Nominal)

Source: CBN, Bruegel

The balance-of-payments data are consistent with that picture. Nigeria recorded a $12.1 billion current-account surplus in the first nine months of 2025, helped by a strong oil-led goods surplus and large remittance-related inflows. However, non-oil trade remained in deficit, while services and primary income stayed deeply negative. Though gross external reserves rose to about $50billion in February 2026 with net reserves at $35billion at the end of 2025, a look at Nigeria’s Net International Investment Position (NIIP) provides more insights. The NIIP position was still deeply negative at -$66.4 billion through September 2025. More importantly for the FX story, portfolio investment liabilities were about $44.1 billion, almost the same size as reserve assets around the time, with debt securities alone at about $39.8 billion.

In essence, while the exchange rate is now broadly competitive, Nigeria’s external position remains vulnerable to portfolio-flow reversals. While the reforms have restored price discovery, Nigeria remains too heavily reliant on high-yield inflows for stability. Without a doubt, he current account surplus and reserve accumulation are real gains. But they do not resolve whether FX stability is self-sustaining or dependent on reversible conditions—high risk appetite, oil prices, and carry differentials. The next reform stage must look to anchor stability over the medium term.

In what follows we look at six potential areas where policymakers can deliver more lasting reforms. They fall into three functional groups. The first group addresses the monetary and exchange-rate framework: recalibrating the purpose of interest rates and establishing cleaner rules for FX market intervention. The second group targets the supply side of the FX market: building durable, recurring inflows rather than relying on volatile portfolio money. While the third group focuses on market infrastructure and the real-side determinants of competitiveness.

First, stop using OMO as a quasi-external borrowing instrument and recalibrate policy rates to domestic price stability mandate. Nigeria still needs positive real rates while inflation remains high and disinflation is not yet fully entrenched. That case is not in dispute. What is in dispute is the purpose those rates are being asked to serve. At present, CBN’s Open Market Operations (OMO) function partly as a quasi-external borrowing instrument: the rate on OMO bills is set at levels designed to attract and retain offshore portfolio money, and the stability that results is rented from that carry differential. The problem with this arrangement is not the rate level per se — it is the dependency it creates. An OMO-anchored FX stability strategy requires the CBN to keep nominal interest rates elevated even as inflation moderates, because any reduction risks triggering outflows. It also means that domestic monetary transmission — the channel through which interest rate decisions affect credit, investment, and ultimately inflation — is subordinated to the external financing objective. The tail wags the dog.

As inflation moderates, the CBN should gradually shift toward a cleaner corridor-based system in which the policy rate, open market operations, and standing facilities are oriented primarily toward managing Naira liquidity and anchoring domestic expectations. That means the policy rate (26.5%) converges toward the OMO rate (19-20%) rather than being maintained as a separate instrument for external purposes. It also means progressively reducing the excessive reliance on cash reserve requirements, which raise intermediation spreads, weaken monetary transmission, and make tightening more costly than necessary. The transition should be gradual and clearly communicated: the goal is not to abruptly remove the carry differential, but to change the basis on which FX stability is maintained.

Second, make the exchange rate a shock absorber (not a target) and make inflation targeting an explicit objective. Nigeria’s 2023–24 reform moved the exchange rate from a managed peg toward a more flexible arrangement. The next step is to make that flexibility credible by institutionalising how the CBN intervenes — and, crucially, how it does not. In an oil economy, where export earnings are large but volatile, the exchange rate’s role as a shock absorber is particularly important. When oil prices fall, a flexible Naira can take some of the adjustment that would otherwise fall on reserves, fiscal balances, or growth. Preventing that adjustment — by intervening to hold the rate — merely defers and concentrates the shock. A transparent, rules-based intervention framework would be significantly better than the current partially discretionary setup. Markets should know, at least broadly, what conditions trigger CBN’s intervention, what the reserve objective is, and what the central bank is not trying to defend. One way out is inflation targeting. Various CBN governors have adopted the language of inflation targeting — announcing targets, publishing a target band, citing price stability mandates — while in practice pursuing nominal exchange-rate stability as the operating objective.

The result is the worst of both arrangements: the CBN takes on the political costs of a peg without the transparency of one, and the exchange rate loses its capacity to absorb shocks because it is quietly being used as an anchor. The remedy is to make the inflation target explicit, binding, and publicly accountable over a clearly defined horizon — 18 to 24 months is realistic given the current inflation trajectory and the lags in monetary transmission. An explicit target forces the CBN to specify what it is actually trying to achieve with its instruments over that period, which in turn encodes — implicitly but rigorously — the real exchange rate path consistent with stabilising demand and supply in the FX market. Without that anchor, the temptation to manage the nominal rate for short-term stability will reassert itself whenever inflows are strong and the political costs of adjustment are high.

To sharpen market focus, the CBN should follow the practice of peer central banks and publish a preferred operational measure — core inflation, stripping out volatile food and energy components — alongside the headline figure, using the former to signal the underlying trend its instruments are actually targeting. Establishing this framework credibly upfront is also how the CBN addresses the time-inconsistency problem that has historically undermined Nigeria’s monetary policy: committing publicly to a path makes future deviation costly, which is precisely the discipline the framework is designed to create.

Third, move more durable FX supply into the market. In thinking about alternative sources of USD supply outside FPI flows, Nigeria needs longer-term inflows from oil and non-oil exports, direct investments and remittances. Beyond portfolio flows, Nigeria has three durable sources of autonomous FX supply that remain structurally underdeveloped. The first is remittances. Nigeria is already among the world's largest remittance recipients, but a significant share still flows through informal channels that never reach the official FX market. The priority is channel migration rather than volume creation: completing the remote BVN rollout for diaspora Nigerians, aggressively reducing transfer costs by licensing more fintech corridors and dismantling legacy operator protections, and designing diaspora Naira investment accounts that are genuinely competitive on rate and liquidity. A properly structured diaspora bond programme — drawing on the models used by India and Israel — could convert remittance relationships into longer-duration capital flows if the institutional credibility is there to support it.

The second source is non-oil commodity exports, where the gap between Nigeria's production potential and its realised dollar earnings is large and closeable. Nigeria is a significant global producer of cocoa, sesame, cashew, ginger, and rubber, and sits on substantial untapped deposits of lithium, gold, and other solid minerals. In agriculture, the constraints are post-harvest infrastructure, quality certification, and the trade finance access that would allow smallholder cooperatives to scale. In solid minerals, the dominant problem is informality: artisanal miners export gold and lithium through unofficial channels into neighbouring countries or directly to Gulf and Asian buyers, generating no official FX supply. Across both sectors, repatriation enforcement is the binding constraint: the rules exist, but tying export licence renewal and trade finance access to verified repatriation compliance — with actual penalties — remains inconsistently applied.

The third source is industrial exports, where the instrument is deliberate policy rather than market development. Special economic zones and industrial parks, properly resourced with reliable power, streamlined export procedures, and competitive logistics, can attract the manufacturing investment that generates recurring export proceeds. None of this is strictly central banking work, but the CBN can drive meaningful coordination here by directing development finance institutions — the Bank of Industry, the NEXIM Bank, and multilateral partners including the AfDB and Afreximbank — toward trade finance facilities, processing infrastructure, and export-credit schemes that unlock these flows. The CBN's convening authority across fiscal, regulatory, and financing actors is an underused instrument. Deploying it deliberately in support of non-oil export development would be one of the most structurally significant contributions it could make to FX market deepening.

Fourth, route oil-related inflows through the official market more systematically. Oil remains Nigeria’s dominant source of foreign currency, and how those earnings enter the FX market matters enormously for market depth and price discovery. At present, a significant share of oil-related FX flows through administrative channels rather than the official market, which concentrates supply in the CBN rather than distributing it through market participants. The medium-term objective should be a rules-based system in which a larger share of oil-related FX is sold through NAFEM. Where the CBN wishes to accumulate reserves, it should do so transparently through market purchases rather than through opaque administrative capture of export receipts. This might require legal amendments and/or executive orders which dictate how various Nigerian agencies (NNPC, NRS, NUPRC, NMDPRA) collect and remit dollars into the Federation Account. Critically, it also changes the FX supply dynamic from one where the central bank is the dominant and discretionary supplier to one where supply is more distributed, more predictable, and more responsive to market conditions.

Fifth, deepen domestic market-making capacity. A deep FX market is not one where the central bank supplies every marginal dollar on demand. It is one where banks, exporters, remitters, and end-users can warehouse some risk, trade across time, and provide liquidity to each other without requiring continuous central bank intervention. Building that capacity is a medium-term project, but the policy prerequisites can be put in place now. The most direct lever is allowing banks to hold somewhat larger FX net open positions within prudential limits. Currently, tight NOP constraints reduce banks’ capacity to act as market-makers, which concentrates market risk in the CBN and reduces the resilience of the market to short-term imbalances. Widening NOP limits modestly — within a clear macroprudential framework — would allow banks to provide more intermediation, smooth day-to-day volatility, and reduce the frequency with which CBN intervention is needed to maintain basic market function. Over time, this also lays the groundwork for a more active FX derivatives market, which would allow exporters and importers to hedge currency exposure and reduce the demand for spot dollars that arises from uncertainty about future rates.

Sixth, protect real competitiveness by lowering inflation from the supply side too. This part is easy to miss, but it is central. As shown above, the real competitiveness gains from Naira’s nominal adjustment are already being eroded by high domestic inflation. The exchange rate can be nominally flexible and still lose real competitiveness if the domestic price level rises faster than the rate depreciates. That is the dynamic Nigeria faces if inflation is not brought down from the supply side as well as through monetary tightening.

Monetary policy can anchor inflation expectations and slow demand, but it cannot reduce the cost of food transport, lower import barriers on agricultural inputs, or fix the power supply failures that raise production costs across the economy. Those are fiscal, regulatory, and infrastructure policy levers. But the connection to FX policy is direct: high domestic inflation forces Nigeria to offer very large nominal yields to attract portfolio inflows, which in turn creates the OMO dependency. Lower structural inflation would allow lower nominal yields, reduce the carry-trade dependency, and permit the exchange rate to be more genuinely market-determined. Trade policy, logistics investment, conflict resolution along trade corridors, and productivity growth in tradable sectors are therefore not separate from the FX reform agenda. They are part of it. Using CBN’s convening power for coordination across different policy domains will thus be crucial.

Conclusion

Nigeria’s first phase of monetary reforms was an act of correction. After years of overvaluation, administrative rationing, and the distortions that came with them, the 2023–24 reforms restored a basic market logic to the foreign exchange system. That was necessary and significant. But it is not sufficient.

The diagnosis presented here suggests a specific vulnerability: the exchange rate is now broadly competitive, but the external balance sheet — with portfolio liabilities nearly matching reserve assets and a deeply negative NIIP — remains exposed to flow reversals. Competitiveness gains are eroding through domestic inflation. FX stability is still too dependent on maintaining high carry differentials, which subordinates domestic monetary policy to external financing conditions and limits the exchange rate’s capacity to function as a genuine shock absorber.

The six reforms proposed here address these vulnerabilities as a system. Recalibrating OMO rates and deepening market-making capacity will change the basis of stability from rented to earned. Transparent intervention rules and a genuine float will make the exchange rate do the work it is designed to do in an oil economy. Building durable autonomous FX supply — through remittances, export-proceeds repatriation, and better routing of oil inflows — will reduce the market’s dependence on hot money. And addressing supply-side inflation will close the loop between monetary policy, real competitiveness, and the FX framework.

None of this is straightforward. Each reform requires sustained institutional effort and political tolerance for adjustment. But the alternative — drifting back toward implicit pegs, excessive OMO reliance, and a carry-trade-dependent stability — recreates the vulnerabilities that made the 2023–24 correction necessary in the first place. The question is not whether Nigeria needs a second phase of FX reform. It is whether the institutional momentum from the first phase can be converted, deliberately and quickly, into the structural changes that the second phase demands.

Glossary of terms

Carry trade / carry spread: the extra return that foreign investors earn by buying high-yield Naira assets instead of lower-yield foreign assets, so long as the Naira does not weaken too much. In the piece, “yield premium” is even cleaner than “carry spread.”

OMO bills: short-term CBN bills used to absorb excess Naira liquidity from the banking system.

Price discovery: allowing the exchange rate to be determined by buyers and sellers in the market, rather than by official fixing or rationing.

Market depth: an FX market with enough buyers, sellers and intermediaries to absorb shocks without wild swings or constant central bank support.

Net open position: the amount of foreign-exchange risk that banks are allowed to hold on their own balance sheets.

REER/real competitiveness: the inflation-adjusted value of the Naira against the currencies of trading partners. It is a better guide to competitiveness than the nominal exchange rate alone.

NIIP: Stands for Net International Investment Position. In this instance, it stands for Nigeria’s external balance sheet — what Nigerians own abroad minus what foreigners own in Nigeria.